Philips 2004 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2004 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

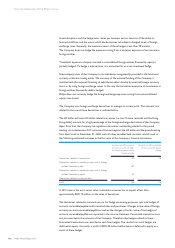

A sensitivity analysis shows that if long-term interest rates were to decrease instantaneously by

1% from their level of December 31, 2004, with all other variables (including foreign exchange

rates) held constant, the fair value of the long-term debt would increase by approximately

EUR 169 million. This increase is based on the assumption that the ‘putable’ bonds will be

repaid at their final maturity date. Assuming bondholders required payment at their respective

put dates, if there was an increase in interest rates by 1%, this would reduce the market value of

the long-term debt by approximately EUR 135 million.

If interest rates were to increase instantaneously by 1% from their level of December 31, 2004,

with all other variables held constant, the net interest expense would decrease by

approximately EUR 28 million in 2005 due to the significant cash position of the Company. This

impact is based on the outstanding position at year-end.

Liquidity risk

The rating of the Company’s debt by major rating services may improve or deteriorate. As a

result, the Company’s borrowing capacity may be influenced and its financing costs may

fluctuate. The EUR 4,349 million in cash and short-term deposits and the USD 2,500 million

stand-by facility mitigate the liquidity risk for the Company.

Equity price risk

Philips is a shareholder in several publicly listed companies such as TSMC, LG.Philips LCD,

NAVTEQ, FEI, Atos Origin, JDS Uniphase and GN Great Nordic. As a result, Philips is exposed

to equity price risk through movements in the share prices of these companies. The aggregate

equity price exposure of these investments amounted to approximately EUR 10,950 million at

year-end 2004 (2003: 8,290 million including shares that were sold during 2004).

Commodity price risk

The Company is a purchaser of certain base metals (such as copper), precious metals and

energy. The Company hedges certain commodity price risks using derivative instruments to

minimize significant, unanticipated earnings fluctuations caused by commodity price volatility.

The commodity price derivatives that the Company enters into are concluded as cash flow

hedges to offset forecasted purchases. A 10% increase in the market price of all commodities

would increase the fair value of the derivatives by EUR 1 million.

Credit risk

Credit risk represents the loss that would be recognized at the reporting date if counterparties

failed completely to perform their payment obligations as contracted. As of December 31,

2004, there are no individual customers with significant outstanding receivables. To reduce

exposure to credit risk, the Company performs ongoing credit evaluations of the financial

condition of its customers and adjusts payment terms and credit limits when appropriate.

The Company invests available cash and cash equivalents with various financial institutions. The

Company is also exposed to credit risks in the event of non-performance by counterparties

with respect to financial derivative instruments.

The Company measures on a daily basis the potential loss under certain stress scenarios, should

a financial counterparty default. These worst-case scenario losses are monitored and limited by

the Company. As of December 31, 2004 the Company had credit risk exceeding EUR 25 million

to the following number of counterparties:

168 Philips Annual Report 2004

Financial statements of the Philips Group