Philips 2004 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2004 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

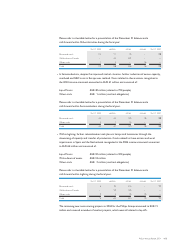

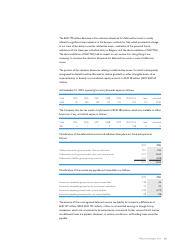

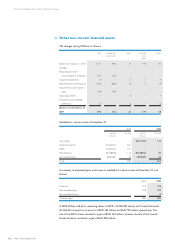

The EUR 170 million decrease in the valuation allowance for deferred tax assets is mainly

related to significant improvements in the business outlook for Italy which prompted a change

in our view of the ability to realize related tax assets, evaluation of the potential future

realization of the claims per individual entity in Belgium, and the deconsolidation of NAVTEQ.

The deconsolidation of NAVTEQ had no impact on net income. For Hong Kong it was

necessary to increase the valuation allowance for deferred tax assets in view of additional

losses.

The portion of the valuation allowance relating to deferred tax assets, for which subsequently

recognized tax benefits will be allocated to reduce goodwill or other intangible assets of an

acquired entity or directly to contributed capital, amounts to EUR 38 million (2003: EUR 53

million).

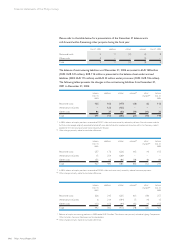

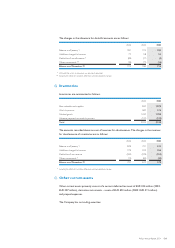

At December 31, 2004, operating loss carryforwards expire as follows:

Total 2005 2006 2007 2008 2009 2010/2014 later unlimited

4,500 30 260 160 100 100 150 370 3,330

The Company also has tax credit carryforwards of EUR 280 million, which are available to offset

future tax, if any, and which expire as follows:

Total 2005 2006 2007 2008 2009 2010/2014 later unlimited

280 51191 22821 14

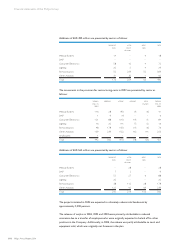

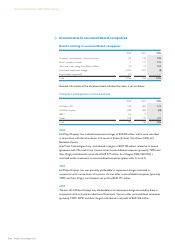

Classification of the deferred tax assets and liabilities takes place at a fiscal entity level as

follows:

2003 2004

Deferred tax assets grouped under other current assets 357 334

Deferred tax assets grouped under other non-current assets 1,417 1,463

Deferred tax liabilities grouped under provisions (157)(228)

1,617 1,569

Classification of the income tax payable and receivable is as follows:

2003 2004

Income tax receivable grouped under current receivables 138 46

Income tax receivable grouped under non-current receivables 19 23

Income tax payable grouped under current liabilities (235) (277)

Income tax payable grouped under non-current liabilities (78) (74)

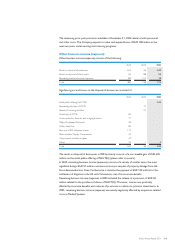

The amount of the unrecognized deferred income tax liability for temporary differences of

EUR 141 million (2003: EUR 152 million), relates to unremitted earnings in foreign Group

companies, which are considered to be permanently re-invested. Under current Dutch tax law,

no additional taxes are payable. However, in certain jurisdictions, withholding taxes would be

payable.

123Philips Annual Report 2004