Philips 2004 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2004 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

litigation cannot be determined due to a number of variables, the

Company’s financial position and results of operations could be

affected by an adverse outcome. Please refer to note 26 of the

consolidated financial statements for the disclosed litigation

matters.

Philips has defined-benefit pension plans in a number of

countries. The cost of maintaining these plans is influenced

by fluctuating macro-economic and demographic

developments, creating volatility in Philips’ results.

The majority of employees in Europe and North America are

covered by these plans. The accounting for defined-benefit pension

plans requires management to make assumptions regarding

variables such as discount rate, rate of compensation increase and

expected return on plan assets.

Changes in these assumptions can have a significant impact on the

projected benefit obligations, funding requirements and periodic

pension cost. A negative performance of the capital markets could

have a material impact on pension expense and on the value of

certain financial assets of the Company. For a discussion of

pension-related exposure to changes in financial markets, please

refer to the sensitivity analysis presented hereafter, and for

quantitative and qualitative disclosure of pensions, please refer to

note 20 of the consolidated financial statements.

Pension-related exposure to changes in financial

markets

With pension obligations in more than forty countries, the

Company has devoted considerable attention and resources to

ensuring disclosure, awareness and control of the resulting

exposures.

Depending on the investment policies of the respective pension

funds, the value of pension assets compared to the related pension

liabilities, and the composition of such assets, developments in

financial markets may have a significant effect on the funded status

of the Company’s pension plans and their related pension cost. To

monitor the corresponding risk exposure, a ‘Global Risk Reward

Model’ for pensions has been developed. The model, which covers

approximately 95% of total pension liabilities and contains separate

modules for the Netherlands, the UK, the US and Germany, allows

estimates of the sensitivities to changes in equity market valuations

and interest rates.

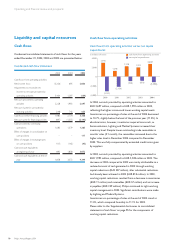

The bar charts in the sections hereafter show the estimated

sensitivities to interest rates and equity market valuations for the

Netherlands, the UK, the US and Germany, on aggregate, based

upon the assets, liabilities, discount rates and asset allocations as of

December 31, 2004. They show how much the aggregate funded

status and additional minimum liability would have differed from

what they actually were, if interest rates or equity valuations had

been lower or higher, and to what extent net periodic pension

cost (NPPC) for 2005 would have been affected. All results are

shown as a percentage of total projected benefit obligations (PBO,

amounting to EUR 19.5 billion) or total NPPC (estimated to be

EUR 235 million). The interest rate sensitivities have been

estimated on the assumption that interest rates and discount rates

change simultaneously. The estimated sensitivities presented do

not reflect the correlation, if any, between changes in interest

rates and equity market valuations.

Funded status

A change in interest rates affects the values of both assets and

liabilities, whereas changes in equity valuations affect asset values

only. Generally speaking, the interest rate sensitivity of the

liabilities tends to be significantly greater than the sensitivity of

pension assets. Consequently, decreases in interest rates tend to

have detrimental effects on the funded status of a plan.

As of December 31, 2004, for Company-sponsored plans, 57% of

pension assets were invested in fixed-income securities, an

increase of 9% over the prior year. There was a corresponding

decrease in equity securities. This change was a result of actions

taken by the Dutch pension fund to reduce its interest rate

sensitivity. Although in relative terms the sensitivity of the Dutch

pension plan’s funded status is lower than the sensitivity of other

major Company-sponsored plans, due to the relative size of its

pension liabilities (which cover 64% of the total PBO for the

Company), the interest rate risk for the Dutch pension plan

compared to the Company’s total pension obligations is still larger

than that for the other countries.

79Philips Annual Report 2004