Philips 2004 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2004 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

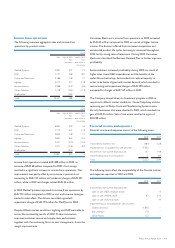

Semiconductors

Key data

in millions of euros 2002 2003 2004

Sales 5,032 4,988 5,464

Sales growth

% (decrease) increase, nominal (1) (1) 10

% increase, comparable 2 11 13

Income (loss) from operations (524) (342) 450

asa%ofsales (10.4) (6.9) 8.2

Net operating capital (NOC) 3,814 2,676 2,669

Employees (FTEs) 34,225 33,177 35,116

See pages 210 and 211 for a reconciliation to the most directly comparable US GAAP measures.

Sales and net operating capital

8

10

6

4

2

0

in billions of euros sales NOC

20042003200220012000

5.0

6.8

5.0

5.1 5.5

Income from operations

1,453

450

(716) (524) (342)

2,000

1,500

1,000

500

0

(500)

(1,000)

in millions of euros as a % of sales

30%

40%

20%

10%

0%

(10%)

(20%)

20042003200220012000

Market developments

Fueled by the performance of the US and Chinese economies and

following the recovery started in the second half of 2003, the

semiconductor markets peaked in 2004 with 28% growth in

US dollar terms. However, with rising US interest rates and

growing concerns about the recovery, order books were

shortened during the second half of the year, leading to a general

decline of technology markets. The sharp fall in panel prices in the

third quarter of 2004 and pressure on LCD TV prices, as well as

price declines in the mobile phone market in the face of strong

competition from Chinese brands, adversely affected results in the

second half. The market for standard products also grew faster in

the first half, as the sector peaked, declining afterwards in line with

order books. The mobile phone market ended the year at a level

of 650 million handsets. The mobile displays market experienced a

continuous shift from monochrome to color, the latter now

accounting for more than 80% of the market.

Strategy

Serving the consumer, communication, automotive and computing

markets, Semiconductors is actively managing a balanced portfolio

spanning emerging, mature and multi-market products. The focus

is on the development of Nexperia-based customer solutions that

combine semiconductors, software and services. In this respect

the division aims to grow particularly in DVD+RW, LCD TV and

communication products. The focus on key accounts continues.

Semiconductors has adopted a capital-efficient manufacturing

strategy in order to be more flexible and effective throughout

future industry cycles. Having rationalized its own wafer capacity,

it expects to continue to outsource a large percentage of future

capacity needs during upturns and load its own manufacturing sites

with stable products. In 2004, the division reduced R&D costs as a

percentage of sales, while continuing to invest in its technology

partnership with STMicroelectronics and Freescale at Crolles2.

Financial performance

2004 was the best year for the semiconductor markets since the

peak year of 2000, with a strong first three quarters of the year.

Semiconductors’ share of the markets it serves was relatively

stable compared to 2003. Continuing the trend of 2003, capacity

utilization rose in the first half of 2004 to 99%, but declined to 81%

in the fourth quarter. Consumer and Mobile Communications

posted strong growth, while margins improved at Mobile Display

Systems and for standard products.

55Philips Annual Report 2004