APC 2013 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2013 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

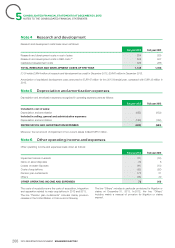

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

|

|

5CONSOLIDATED FINANCIALSTATEMENTS ATDECEMBER 31, 2013

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Accounting Policies

Note1

1.1 – Accounting standards IFRS12 – Disclosure of Interests in Other entities,

l

Investment Entities – Amendments to IFRS10, IFRS12 and

l

The consolidated financial statements have been prepared in

IAS27,

compliance with the international accounting standards (IFRS) as which application is required from January1, 2013 under

adopted by the European Union as of December31, 2013. IFRSas issued by IASB but which application is mandatory only

Thesame accounting methods were used as for the from January1, 2014 as per the European Union.

consolidated financial statements for the year ended At this stage of analysis, the Group does not expect other

December31, 2012. impact, on its consolidated financial statements, to be material.

The following standards and interpretations that were applicable

Restated 2012 comparative consolidated 1.2 –

during the period did not have a material impact on the

consolidated financial statements as of December31, 2013:

IFRS13 – Fair value Measurement;

lfinancial statements

amendment to IAS1 – Presentation of Items of Other

lThe Group has been applying IAS19 revised since January1,

Comprehensive Income, 2013 with retroactive effect from January1, 2012 on

amendment to IAS12 – Recovery of Underlying Assets,

lcomparative financial statements. In accordance with IAS19

improvements to IFRSs 2009-2011 (May2012),

lrevised requirements published on June2011, the expected

amendments to IFRS7 – Disclosures – Transfer of Financial

lreturn on long term plan assets in 2013 is equal to discount rate

assets.at December31, 2012 closing date. The effect in 2013 is

Additionally, IAS19 revised was applied from January1, 2013 EUR40million as a reduction of financial income and is also

with retroactive effect from January1, 2012 on 2012 EUR39million as a reduction of financial income in 2012; the

comparative financials which impacts are detailed in note1.2. difference between the actual rate and the rate assessed this

The Group did not apply the following standards and way is booked as non recycled OCI.

interpretations that are mandatory at some point subsequent to Moreover, IAS19 revised requires the recycling through equity of

December31, 2013: past service costs, of which the amortization was a gain of about

standards adopted by the European Union:

lEUR1million per year, that will have an expected effect of

EUR17million at January1, 2013. 2012 figures were restated by

IAS28 revised – Investments in associates and

–

applying IAS19 revised, with:

joint-ventures,

amendment to IAS32 – Offsetting Financial assets and

–an increase in consolidated retained earnings of EUR12million

l

Financial liabilities,on January1, 2012,

IFRS10 – Consolidated Financial Statements,

–a cost after tax of EUR27million on 2012 net income,and

l

IFRS11 – Joint Arrangements,

–a profit net of tax of EUR26million on 2012 OCI.

l

IFRS12 – Disclosure of Interests in Other entities,

–IAS19 Revised has no effect on the recognition of actuarial gains

& losses since those were already directly recognized in equity.

Transition Guidance – amendments to IFRS10, IFRS11

–

and IFRS12,

Basis of presentation1.3 –

amendment to IAS36 – Recoverable amount disclosures for

–

non-financial assets,

The financial statements have been prepared on a historical cost

amendment to IAS39 – Novation of derivatives and

–

basis, with the exception of derivative instruments and available –

continuation of hedge accounting,

for-sale financial assets, which are measured at fair value.

Investment Entities – amendments to IFRS10, IFRS12 and

–

Financial liabilities are measured using the amortized cost model.

IAS27,

The book value of hedged assets and liabilities, under fair-value

standards not yet adopted by the European Union:

l

hedge, corresponds to their fair value, for the part corresponding

IFRS9 – Financial instruments,

–to the hedged risk.

improvements to IFRSs 2010-2012 (December2013),

–

Use of estimates and assumptions1.4 –

improvements to IFRSs 2011-2013 (December2013),

–

IFRIC21 – Levies.

–

There are no differences in practice between the standards The preparation of financial statements requires Group and

applied by Schneider Electric as of December31, 2013 and the subsidiary management to make estimates and assumptions

IFRSissued by the International Accounting Standards board that are reflected in the amounts of assets and liabilities reported

(IASB), except for: in the consolidated balance sheet, the revenues and expenses in

IAS28 revised – Investments in associates and joint-ventures,

lthe statement of income and the obligations created during the

IFRS10 – Consolidated Financial Statements,

lreporting period. Actual results may differ.

IFRS11 – Joint Arrangements,

l

190 2013 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC