Coca Cola 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

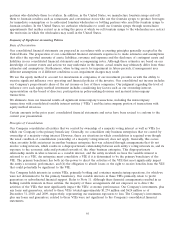

Certain events or changes in circumstances may indicate that the recoverability of the carrying amount of property,

plant and equipment should be assessed, including, among others, a significant decrease in market value, a significant

change in the business climate in a particular market, or a current period operating or cash flow loss combined with

historical losses or projected future losses. When such events or changes in circumstances are present, we estimate the

future cash flows expected to result from the use of the asset (or asset group) and its eventual disposition. These

estimated future cash flows are consistent with those we use in our internal planning. If the sum of the expected future

cash flows (undiscounted and without interest charges) is less than the carrying amount, we recognize an impairment

loss. The impairment loss recognized is the amount by which the carrying amount exceeds the fair value. We use a

variety of methodologies to determine the fair value of property, plant and equipment, including appraisals and

discounted cash flow models, which are consistent with the assumptions we believe hypothetical marketplace

participants would use. Refer to Note 7.

Goodwill, Trademarks and Other Intangible Assets

We classify intangible assets into three categories: (1) intangible assets with definite lives subject to amortization,

(2) intangible assets with indefinite lives not subject to amortization and (3) goodwill. We determine the useful lives of

our identifiable intangible assets after considering the specific facts and circumstances related to each intangible asset.

Factors we consider when determining useful lives include the contractual term of any agreement related to the asset,

the historical performance of the asset, the Company’s long-term strategy for using the asset, any laws or other local

regulations which could impact the useful life of the asset, and other economic factors, including competition and

specific market conditions. Intangible assets that are deemed to have definite lives are amortized, primarily on a

straight-line basis, over their useful lives, generally ranging from 1 to 20 years. Refer to Note 8.

When facts and circumstances indicate that the carrying value of definite-lived intangible assets may not be recoverable,

management assesses the recoverability of the carrying value by preparing estimates of sales volume and the resulting

gross profit and cash flows. These estimated future cash flows are consistent with those we use in our internal planning.

If the sum of the expected future cash flows (undiscounted and without interest charges) is less than the carrying

amount, we recognize an impairment loss. The impairment loss recognized is the amount by which the carrying amount

exceeds the fair value. We use a variety of methodologies to determine the fair value of these assets, including

discounted cash flow models, which are consistent with the assumptions we believe hypothetical marketplace

participants would use.

We test intangible assets determined to have indefinite useful lives, including trademarks, franchise rights and goodwill,

for impairment annually, or more frequently if events or circumstances indicate that assets might be impaired. Our

Company performs these annual impairment reviews as of the first day of our third fiscal quarter. We use a variety of

methodologies in conducting impairment assessments of indefinite-lived intangible assets, including, but not limited to,

discounted cash flow models, which are based on the assumptions we believe hypothetical marketplace participants

would use. For indefinite-lived intangible assets, other than goodwill, if the carrying amount exceeds the fair value, an

impairment charge is recognized in an amount equal to that excess.

We perform impairment tests of goodwill at our reporting unit level, which is one level below our operating segments.

Our operating segments are primarily based on geographic responsibility, which is consistent with the way management

runs our business. Our operating segments are subdivided into smaller geographic regions or territories that we

sometimes refer to as business units. These business units are also our reporting units. The Bottling Investments

operating segment includes all Company-owned or consolidated bottling operations, regardless of geographic location,

except for bottling operations managed by CCR which are included in our North America operating segment.

Generally, each Company-owned or consolidated bottling operation within our Bottling Investments operating segment

is its own reporting unit. Goodwill is assigned to the reporting unit or units that benefit from the synergies arising from

each business combination. In 2010, the Company combined several reporting units within our Europe operating

segment. In addition, we also combined several reporting units within our Pacific operating segment. These changes

were the result of the Company’s productivity initiatives.

The goodwill impairment test consists of a two-step process, if necessary. The first step is to compare the fair value of a

reporting unit to its carrying value, including goodwill. We typically use discounted cash flow models to determine the

fair value of a reporting unit. The assumptions used in these models are consistent with those we believe hypothetical

marketplace participants would use. If the fair value of the reporting unit is less than its carrying value, the second step

98