Coca Cola 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

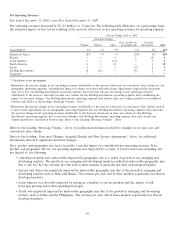

growth in 2010. The group’s strong marketing initiatives, including our FIFA World Cup activation programs,

contributed to the unit case volume growth in North America.

The volume and net operating revenues attributable to the sale of DPS brands have been included as a structural

change in our analysis of net operating revenues. Refer to the heading ‘‘Net Operating Revenues,’’ below, and

‘‘Structural Changes and New License Agreements,’’ above.

In Pacific, unit case volume increased 6 percent, which consisted of 13 percent growth in still beverages and 2 percent

growth in sparkling beverages. The group’s volume growth was led by 6 percent growth in China, 15 percent growth in

the Philippines and 3 percent growth in Japan. China’s volume growth included 21 percent growth in juices and juice

drinks primarily due to the continued strong momentum of Minute Maid Pulpy, as well as strong growth in other still

beverages including water. Tough weather conditions, including flooding in the higher per capita consumption regions,

negatively impacted unit case volume in China. In the Philippines, unit case volume growth was led by 14 percent

growth in Trademark Coca-Cola. In Japan, the unit case volume growth was driven by successful in-market activations,

strong innovation and favorable weather conditions. Included in Japan’s unit case volume growth was 5 percent growth

in Trademark Coca-Cola, primarily due to strong FIFA World Cup activation programs and our Coca-Cola Summer

Promotion. Japan’s unit case volume growth also benefited from 17 percent growth in sports drinks.

Unit case volume for Bottling Investments decreased 1 percent, primarily due to the deconsolidation of certain entities

as a result of the Company’s adoption of new accounting guidance issued by the FASB. These entities are primarily

bottling operations and have been accounted for under the equity method of accounting since they were deconsolidated

on January 1, 2010. Refer to the heading ‘‘Critical Accounting Policies and Estimates — Principles of Consolidation’’

and ‘‘Structural Changes, Acquired Brands and New License Agreements.’’ The deconsolidation of these entities

negatively impacted the unit case volume for Bottling Investments by approximately 9 percent. Unit case volume for

Bottling Investments was also negatively impacted by the sale of our Norwegian and Swedish bottling operations to New

CCE. The unfavorable impact of the aforementioned items was partially offset by growth in markets where we own or

otherwise consolidate the bottling operations. Unit case volume grew 6 percent in China, 17 percent in India,

15 percent in the Philippines and 1 percent in Germany. The Company’s consolidated bottling operations account for

approximately 33 percent, 66 percent, 100 percent and 100 percent of the unit case volume in China, India, the

Philippines and Germany, respectively.

Year Ended December 31, 2009, versus Year Ended December 31, 2008

In Eurasia and Africa, unit case volume increased 4 percent, which consisted of 3 percent growth in sparkling beverages

and 8 percent growth in still beverages. The group’s unit case volume growth was primarily attributable to 31 percent

growth in India, led by 32 percent growth in sparkling beverages. The sparkling beverages growth in India was largely

due to double-digit growth in Trademarks Thums Up, Sprite, Fanta and Coca-Cola. Still beverages in India grew

28 percent, driven by double-digit growth in Trademark Maaza. The group also benefited from 6 percent volume growth

in North and West Africa and 10 percent volume growth in East and Central Africa. The group’s unit case volume

growth also included the impact of a 14 percent volume decline in Russia, primarily due to a challenging economic

environment. In addition, South Africa and Turkey each experienced a 1 percent unit case volume decline.

Unit case volume in Europe decreased 1 percent, primarily attributable to difficult macroeconomic conditions

throughout most of Europe. These difficult macroeconomic conditions impacted a number of key markets and

contributed to unit case volume declines of 8 percent in South and Eastern Europe, 4 percent in Iberia and 2 percent

in Germany. The volume declines in these markets were partially offset by 6 percent unit case volume growth in France

and 4 percent growth in Great Britain. The unit case volume growth in both France and Great Britain was led by

Trademark Coca-Cola.

In Latin America, unit case volume increased 6 percent, which consisted of 3 percent growth in sparkling beverages and

24 percent growth in still beverages. The group benefited from strong volume growth in key markets, including

6 percent in Mexico, 4 percent in Brazil, 2 percent in Argentina and double-digit growth in Colombia. Acquisitions

contributed 1 percentage point of the group’s total unit case volume growth. The group’s sparkling beverage volume

growth was primarily attributable to 4 percent growth in brand Coca-Cola. The successful integration of Jugos del

Valle, S.A.B. de C.V. (‘‘Jugos del Valle’’) drove still beverage volume growth.

56