Coca Cola 2010 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

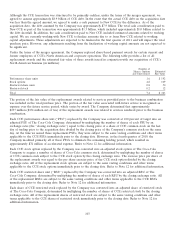

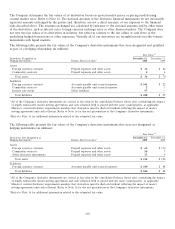

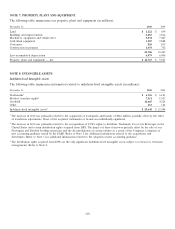

NOTE 4: INVENTORIES

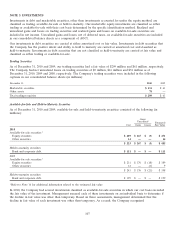

Inventories consist primarily of raw materials and packaging (which includes ingredients and supplies) and finished

goods (which include concentrates and syrups in our concentrate operations, and finished beverages in our finished

products operations). Inventories are valued at the lower of cost or market. We determine cost on the basis of the

average cost or first-in, first-out methods. Inventories consisted of the following (in millions):

December 31, 2010 2009

Raw materials and packaging $ 1,425 $ 1,366

Finished goods 1,029 697

Other 196 291

Total inventories $ 2,650 $ 2,354

NOTE 5: HEDGING TRANSACTIONS AND DERIVATIVE FINANCIAL INSTRUMENTS

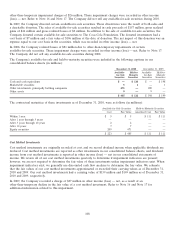

The Company is directly and indirectly affected by changes in certain market conditions. These changes in market

conditions may adversely impact the Company’s financial performance and are referred to as ‘‘market risks.’’ Our

Company, when deemed appropriate, uses derivatives as a risk management tool to mitigate the potential impact of

certain market risks. The primary market risks managed by the Company through the use of derivative instruments are

foreign currency exchange rate risk, commodity price risk and interest rate risk.

The Company uses various types of derivative instruments including, but not limited to, forward contracts, commodity

futures contracts, option contracts, collars and swaps. Forward contracts and commodity futures contracts are

agreements to buy or sell a quantity of a currency or commodity at a predetermined future date, and at a

predetermined rate or price. An option contract is an agreement that conveys the purchaser the right, but not the

obligation, to buy or sell a quantity of a currency or commodity at a predetermined rate or price during a period or at

a time in the future. A collar is a strategy that uses a combination of options to limit the range of possible positive or

negative returns on an underlying asset or liability to a specific range, or to protect expected future cash flows. To do

this, an investor simultaneously buys a put option and sells (writes) a call option. A swap agreement is a contract

between two parties to exchange cash flows based on specified underlying notional amounts, assets and/or indices. We

do not enter into derivative financial instruments for trading purposes.

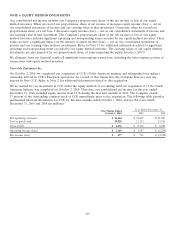

All derivatives are carried at fair value in the consolidated balance sheets in the line items prepaid expenses and other

assets or accounts payable and accrued expenses, as applicable. The carrying values of the derivatives reflect the impact

of legally enforceable master netting agreements and cash collateral held or placed with the same counterparties, as

applicable. These master netting agreements allow the Company to net settle positive and negative positions (assets and

liabilities) arising from different transactions with the same counterparty.

The accounting for gains and losses that result from changes in the fair values of derivative instruments depends on

whether the derivatives have been designated and qualify as hedging instruments and the type of hedging relationships.

Derivatives can be designated as fair value hedges, cash flow hedges or hedges of net investments in foreign operations.

The changes in the fair values of derivatives that have been designated and qualify for fair value hedge accounting are

recorded in the same line item in the consolidated statements of income as the changes in the fair values of the hedged

items attributable to the risk being hedged. The changes in fair values of derivatives that have been designated and

qualify as cash flow hedges or hedges of net investments in foreign operations are recorded in AOCI and are

reclassified into the line item in the consolidated income statement in which the hedged items are recorded in the same

period the hedged items affect earnings. Due to the high degree of effectiveness between the hedging instruments and

the underlying exposures being hedged, fluctuations in the value of the derivative instruments are generally offset by

changes in the fair values or cash flows of the underlying exposures being hedged. The changes in fair values of

derivatives that were not designated and/or did not qualify as hedging instruments are immediately recognized into

earnings.

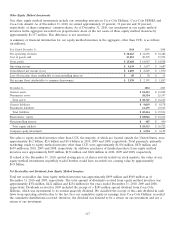

For derivatives that will be accounted for as hedging instruments, the Company formally designates and documents, at

inception, the financial instrument as a hedge of a specific underlying exposure, the risk management objective and the

strategy for undertaking the hedge transaction. In addition, the Company formally assesses, both at the inception and at

least quarterly thereafter, whether the financial instruments used in hedging transactions are effective at offsetting

changes in either the fair values or cash flows of the related underlying exposures. Any ineffective portion of a financial

instrument’s change in fair value is immediately recognized into earnings.

109