Coca Cola 2010 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

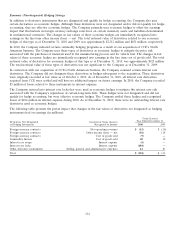

Credit Risk Associated with Derivatives

We have established strict counterparty credit guidelines and enter into transactions only with financial institutions of

investment grade or better. We monitor counterparty exposures regularly and review any downgrade in credit rating

immediately. If a downgrade in the credit rating of a counterparty were to occur, we have provisions requiring collateral

in the form of U.S. government securities for substantially all of our transactions. To mitigate presettlement risk,

minimum credit standards become more stringent as the duration of the derivative financial instrument increases. In

addition, the Company’s master netting agreements reduce credit risk by permitting the Company to net settle for

transactions with the same counterparty. To minimize the concentration of credit risk, we enter into derivative

transactions with a portfolio of financial institutions. Based on these factors, we consider the risk of counterparty

default to be minimal.

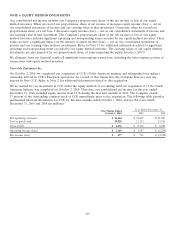

Cash Flow Hedging Strategy

The Company uses cash flow hedges to minimize the variability in cash flows of assets or liabilities or forecasted

transactions caused by fluctuations in foreign currency exchange rates, commodity prices or interest rates. The changes

in the fair values of derivatives designated as cash flow hedges are recorded in AOCI and are reclassified into the line

item in the consolidated income statement in which the hedged items are recorded in the same period the hedged items

affect earnings. The changes in fair values of hedges that are determined to be ineffective are immediately reclassified

from AOCI into earnings. The Company did not discontinue any cash flow hedging relationships during the years ended

December 31, 2010 and 2009. The maximum length of time over which the Company hedges its exposure to future cash

flows is typically three years.

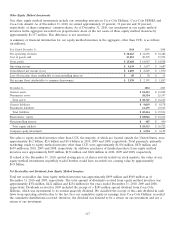

The Company maintains a foreign currency cash flow hedging program to reduce the risk that our eventual U.S. dollar

net cash inflows from sales outside the United States and U.S. dollar net cash outflows from procurement activities will

be adversely affected by changes in foreign currency exchange rates. We enter into forward contracts and purchase

foreign currency options (principally euros and Japanese yen) and collars to hedge certain portions of forecasted cash

flows denominated in foreign currencies. When the U.S. dollar strengthens against the foreign currencies, the decline in

the present value of future foreign currency cash flows is partially offset by gains in the fair value of the derivative

instruments. Conversely, when the U.S. dollar weakens, the increase in the present value of future foreign currency cash

flows is partially offset by losses in the fair value of the derivative instruments. The total notional value of derivatives

that have been designated and qualify for the Company’s foreign currency cash flow hedging program as of

December 31, 2010 and 2009, was approximately $3,968 million and $3,679 million, respectively.

The Company has entered into commodity futures contracts and other derivative instruments on various commodities to

mitigate the price risk associated with forecasted purchases of materials used in our manufacturing process. The

derivative instruments have been designated and qualify as part of the Company’s commodity cash flow hedging

program. The objective of this hedging program is to reduce the variability of cash flows associated with future

purchases of certain commodities. The total notional value of derivatives that have been designated and qualify under

this program as of December 31, 2010 and 2009, was approximately $28 million and $26 million, respectively.

Our Company monitors our mix of short-term debt and long-term debt. From time to time, we manage our risk to

interest rate fluctuations through the use of derivative financial instruments. The Company had no outstanding

derivative instruments under this hedging program as of December 31, 2010 and 2009.

111