Coca Cola 2010 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

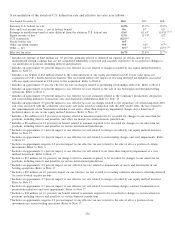

Other Nonoperating Items

Equity Income (Loss) — Net

In 2010, the Company recorded a net charge of $66 million in equity income (loss) — net. This net charge primarily

represents the Company’s proportionate share of unusual tax charges, asset impairments, restructuring charges and

transaction costs recorded by equity method investees. The unusual tax charges primarily relate to an additional tax

liability recorded by Coca-Cola Hellenic Bottling Company S.A. as a result of the Extraordinary Social Contribution Tax

levied by the Greek government. The transaction costs represent our proportionate share of certain costs incurred by

CCE in connection with our acquisition of CCE’s North American business and the sale of our Norwegian and Swedish

bottling operations to New CCE. Refer to Note 2 for additional information related to these transactions. These

charges were partially offset by our proportionate share of a foreign currency remeasurement gain recorded by an

equity method investee. The components of the net charge were individually insignificant. Refer to Note 19 for the

impact these charges had on our operating segments.

During 2009, the Company recorded charges of $86 million in equity income (loss) — net. These charges primarily

represent the Company’s proportionate share of asset impairments and restructuring charges recorded by equity method

investees. Refer to Note 19 for the impact these charges had on our operating segments.

In 2008, the Company recognized a net charge to equity income (loss) — net of $1,686 million, primarily due to our

proportionate share of $7.6 billion of pretax charges ($4.9 billion after-tax) recorded by CCE due to impairments of its

North American franchise rights in the second quarter and fourth quarter of 2008. The Company’s proportionate share

of these charges was $1.6 billion. The decline in the estimated fair value of CCE’s North American franchise rights

during the second quarter was the result of several factors including, but not limited to, (1) challenging macroeconomic

conditions which contributed to lower than anticipated volume for higher-margin packages and certain higher-margin

beverage categories; (2) increases in raw material costs, including significant increases in aluminum, high fructose corn

syrup and resin; and (3) increased delivery costs as a result of higher fuel costs. The decline in the estimated fair value

of CCE’s North American franchise rights during the fourth quarter was primarily driven by financial market conditions

as of the measurement date that caused (1) a dramatic increase in market debt rates, which impacted the capital

charge, and (2) a significant decline in the funded status of CCE’s defined benefit pension plans. In addition, the

market price of CCE’s common stock declined by more than 50 percent between the date of CCE’s interim impairment

test (May 23, 2008) and the date of CCE’s annual impairment test (October 24, 2008). The net charge to equity income

(loss) — net also included a net charge of $60 million, primarily due to our proportionate share of restructuring charges

recorded by our equity method investees. Refer to Note 19 for the impact these charges had on our operating

segments.

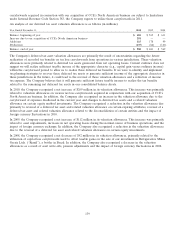

Other Income (Loss) — Net

In 2010, the Company recognized gains of $4,978 million related to the remeasurement of our equity investment in

CCE to fair value, $597 million due to the sale of all of our ownership interests in our Norwegian and Swedish bottling

operations to New CCE and $23 million as a result of the sale of 50 percent of our investment in Le˜

ao Junior, which

was a wholly-owned subsidiary of the Company prior to this transaction. Refer to Note 2 for additional information

related to our acquisition of CCE’s North American business and the sale of all of our ownership interests in our

Norwegian and Swedish bottling operations to New CCE. The gain on the Le˜

ao Junior transaction consisted of two

parts: (1) the difference between the consideration received and 50 percent of the carrying value of our investment and

(2) the fair value adjustment for our remaining 50 percent ownership. We have accounted for our remaining investment

in Le˜

ao Junior under the equity method of accounting since the close of this transaction. The gains related to these

transactions were recorded in other income (loss) — net and impacted our Corporate operating segment. Refer to

Note 16 for fair value disclosures related to these transactions.

During 2010, in addition to the transaction gains, the Company recorded charges of $265 million related to preexisting

relationships with CCE and $103 million due to the remeasurement of our Venezuelan subsidiary’s net assets. The

charges related to preexisting relationships with CCE were primarily due to the write-off of our investment in

infrastructure programs with CCE. Refer to Note 6 for additional information related to our preexisting relationships

with CCE. The remeasurement loss related to our Venezuelan subsidiary’s net assets was due to the Venezuelan

government announcing a currency devaluation and Venezuela becoming a hyperinflationary economy subsequent to

December 31, 2009. As a result, our local subsidiary was required to use the U.S. dollar as its functional currency, and

146