Coca Cola 2010 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

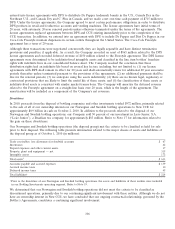

|

bolivars per U.S. dollar prior to the elimination of the official rate for essential goods in December 2010. Prior to the

elimination of the official rate for essential goods, our bottling partner in Venezuela was able to convert bolivars to U.S.

dollars to settle our receivables related to sales approved by the CADIVI. Therefore, as of December 31, 2010, our

receivable balance related to concentrate sales that had been approved by the CADIVI was not significant. If we are

unable to utilize a government-approved exchange rate mechanism for future concentrate sales to our bottling partner

in Venezuela, the amount of receivables related to these sales will increase. In addition, we have certain intangible

assets associated with products sold in Venezuela. If we are unable to utilize a government-approved exchange rate

mechanism for concentrate sales, or if the bolivar further devalues, it could result in the impairment of these intangible

assets. As of December 31, 2010, the carrying value of our accounts receivable from our bottling partner in Venezuela

and intangible assets associated with products sold in Venezuela was approximately $135 million. The revenues and cash

flows associated with concentrate sales to our bottling partner in Venezuela in 2011 are not anticipated to be significant

to the Company’s consolidated financial statements.

Recently Issued Accounting Guidance

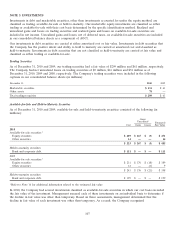

As previously discussed, in June 2009, the FASB amended its guidance on accounting for VIEs. Please refer to the

heading ‘‘Principles of Consolidation,’’ above.

In December 2007, the FASB amended its guidance on accounting for business combinations. The new accounting

guidance resulted in a change in our accounting policy effective January 1, 2009, and is being applied prospectively to

all business combinations subsequent to the effective date. Among other things, the new guidance amends the principles

and requirements for how an acquirer recognizes and measures in its financial statements the identifiable assets

acquired, the liabilities assumed, any noncontrolling interest in the acquiree and the goodwill acquired. It also

establishes new disclosure requirements to enable the evaluation of the nature and financial effects of the business

combination. Refer to Note 2.

In December 2007, the FASB issued new accounting and disclosure guidance related to noncontrolling interests in

subsidiaries (previously referred to as ‘‘minority interests’’), which resulted in a change in our accounting policy effective

January 1, 2009. Among other things, the new guidance requires that a noncontrolling interest in a subsidiary be

accounted for as a component of equity separate from the parent’s equity, rather than as a liability. The new guidance

is being applied prospectively, except for the presentation and disclosure requirements, which have been applied

retrospectively. The adoption of this new accounting policy did not have a significant impact on our consolidated

financial statements.

In December 2007, the FASB issued new accounting guidance that defines collaborative arrangements and establishes

reporting requirements for transactions between participants in a collaborative arrangement and between participants in

the arrangement and third parties. It also establishes the appropriate income statement presentation and classification

for joint operating activities and payments between participants, as well as the sufficiency of the disclosures related to

those arrangements. This new accounting guidance was effective for our Company on January 1, 2009, and its adoption

did not have a significant impact on our consolidated financial statements.

In September 2006, the FASB issued new accounting guidance that defines fair value, establishes a framework for

measuring fair value, and expands disclosure requirements about fair value measurements. However, in February 2008,

the FASB delayed the effective date of the new accounting guidance for all nonfinancial assets and nonfinancial

liabilities, except those that are recognized or disclosed at fair value in the financial statements on a recurring basis (at

least annually), until January 1, 2009. The accounting guidance related to recurring fair value measurements was

effective for our Company on January 1, 2008. The adoption of this accounting guidance did not have a significant

impact on our consolidated financial statements. Refer to Note 16.

101