Coca Cola 2010 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

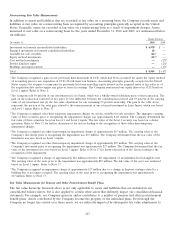

Nonrecurring Fair Value Measurements

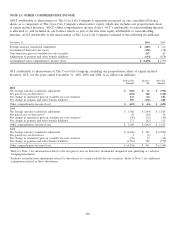

In addition to assets and liabilities that are recorded at fair value on a recurring basis, the Company records assets and

liabilities at fair value on a nonrecurring basis as required by accounting principles generally accepted in the United

States. Generally, assets are recorded at fair value on a nonrecurring basis as a result of impairment charges. Assets

measured at fair value on a nonrecurring basis for the years ended December 31, 2010 and 2009, are summarized below

(in millions):

Gains (Losses)

December 31, 2010 2009

Investment in formerly unconsolidated subsidiary $ 4,9781$—

Retained investment in formerly consolidated subsidiary 122—

Available-for-sale securities (26)3—

Equity method investments (15)4—

Cost method investments —(27)5

Bottler franchise rights —(23)6

Buildings and improvements —(17)7

Total $ 4,949 $ (67)

1The Company recognized a gain on our previously held investment in CCE, which had been accounted for under the equity method

of accounting prior to our acquisition of CCE’s North American business. Accounting principles generally accepted in the United

States require the acquirer to remeasure its previously held noncontrolling equity interest in the acquired entity to fair value as of

the acquisition date and recognize any gains or losses in earnings. The Company remeasured our equity interest in CCE based on

Level 1 inputs. Refer to Note 2.

2The Company sold 50 percent of our investment in Le˜

ao Junior, which was a wholly-owned subsidiary prior to this transaction. The

gain on the transaction consisted of two parts: (1) the difference between the consideration received and 50 percent of the carrying

value of our investment and (2) the fair value adjustment for our remaining 50 percent ownership. The gain in the table above

represents the portion of the total gain related to the remeasurement of our retained investment in Le˜

ao Junior, which was based

on Level 3 inputs. Refer to Note 17.

3The Company recognized other-than-temporary impairment charges on certain available-for-sale securities. The aggregate carrying

value of these securities prior to recognizing the impairment charges was approximately $131 million. The Company determined the

fair value of these securities based on Level 1 and Level 2 inputs. The fair value of the Level 2 security was based on a dealer

quotation. Refer to Note 17 for further discussion of the factors leading to the recognition of these other-than-temporary

impairment charges.

4The Company recognized an other-than-temporary impairment charge of approximately $15 million. The carrying value of the

Company’s investment prior to recognizing the impairment was $15 million. The Company determined that the fair value of the

investment was zero based on Level 3 inputs.

5The Company recognized an other-than-temporary impairment charge of approximately $27 million. The carrying value of the

Company’s investment prior to recognizing the impairment was approximately $27 million. The Company determined that the fair

value of the investment was zero based on Level 3 inputs. Refer to Note 17 for further discussion of the factors leading to the

recognition of the impairment.

6The Company recognized a charge of approximately $23 million related to the impairment of an indefinite-lived intangible asset.

The carrying value of the asset prior to the impairment was approximately $25 million. The fair value of the asset was estimated

based on Level 3 inputs. Refer to Note 17.

7The Company recognized an impairment charge of approximately $17 million due to a change in disposal strategy related to a

building that is no longer occupied. The carrying value of the asset prior to recognizing the impairment was approximately

$17 million. Refer to Note 17.

Fair Value Measurements for Pension and Other Postretirement Benefit Plans

The fair value hierarchy discussed above is not only applicable to assets and liabilities that are included in our

consolidated balance sheets, but is also applied to certain other assets that indirectly impact our consolidated financial

statements. For example, our Company sponsors and/or contributes to a number of pension and other postretirement

benefit plans. Assets contributed by the Company become the property of the individual plans. Even though the

Company no longer has control over these assets, we are indirectly impacted by subsequent fair value adjustments to

143