Coca Cola 2010 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2010 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

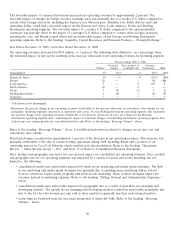

In 2010, the gross profit for our North America operating segment was negatively impacted by $235 million, primarily

due to the elimination of gross profit in inventory on intercompany sales and an inventory fair value adjustment as a

result of the acquisition. Refer to the headings ‘‘Gross Profit Margin’’ and ‘‘Operating Income and Operating Margin.’’

The acquisition of CCE’s North American business has resulted in a significant adjustment to our overall cost structure,

especially in North America. We estimate that approximately 35 percent of our total cost of goods in 2011 will be

comprised of both the raw material and conversion costs associated with the following inputs: (1) sweeteners,

(2) metals, (3) juices and (4) PET. The bulk of these costs will reside within our North America and Bottling

Investments operating segments. We anticipate the underlying commodities related to these inputs will continue to face

upward pressure; and therefore, we have increased our hedging activities related to certain commodities in order to

mitigate a portion of the price risk associated with forecasted purchases. Many of the derivative financial instruments

used by the Company to mitigate the risk associated with these commodity exposures do not qualify for hedge

accounting. As a result, the change in fair value of these derivative instruments will be included as a component of net

income each reporting period. Refer to the heading ‘‘Gross Profit Margin,’’ below, and Note 5 of Notes to Consolidated

Financial Statements for additional information regarding our commodity hedging activity.

The acquisition of CCE’s North American business increased the Company’s selling, general and administrative

expenses in 2010, primarily due to delivery-related expenses. Selling, general and administrative expenses are typically

higher, as a percentage of net operating revenues, for finished products operations compared to concentrate operations.

Selling, general and administrative expenses were also negatively impacted by the amortization of definite-lived

intangible assets acquired in the acquisition. The Company recorded $605 million of definite-lived acquired franchise

rights that are being amortized over a weighted-average life of approximately 8 years, which is equal to the weighted-

average remaining contractual term of the acquired franchise rights. In addition, the Company recorded $380 million of

customer rights that are being amortized over 20 years. We estimate the amortization expense related to these definite-

lived intangible assets to be approximately $100 million per year for the next several years, which will be recorded in

selling, general and administrative expenses.

Once fully integrated, we expect to generate operational synergies of at least $350 million per year. We anticipate

realizing approximately $140 million to $150 million of these synergies in 2011. Refer to the heading ‘‘Other Operating

Charges,’’ below, and Note 18 of Notes to Consolidated Financial Statements for additional information regarding this

integration initiative.

In connection with the Company’s acquisition of CCE’s North American business, we assumed $7,602 million of long-

term debt, which had an estimated fair value of $9,345 million as of the acquisition date. In accordance with accounting

principles generally accepted in the United States, we recorded the assumed debt at its fair value as of the acquisition

date. Refer to Note 2 of Notes to Consolidated Financial Statements.

On November 15, 2010, the Company issued $4,500 million of long-term notes and used some of the proceeds to

repurchase $2,910 million of long-term debt. The Company used the remaining cash from the issuance to reduce our

outstanding commercial paper balance. The repurchased debt consisted of $1,827 million of debt assumed in our

acquisition of CCE’s North American business and $1,083 million of the Company’s debt that was outstanding prior to

the acquisition. The Company recorded a charge of $342 million related to the premiums paid to repurchase the long-

term debt and the costs associated with the settlement of treasury rate locks issued in connection with the debt tender

offer. Refer to the heading ‘‘Interest Expense,’’ below, and Note 10 of Notes to Consolidated Financial Statements for

additional information.

In 2010, we recognized a gain of $4,978 million due to the remeasurement of our equity interest in CCE to fair value

upon the close of the transaction. This gain was classified in the line item other income (loss) — net in our

consolidated statement of income.

Although our 2010 operating results and certain key metrics were affected by these structural changes, we do not

believe it is indicative of the impact they will have on future operating periods. Our 2011 consolidated financial

statements will reflect twelve months of operating results of the acquired CCE North American business and DPS

license agreements compared to three months in 2010. Therefore, we expect these structural changes to have a

significant impact on our operating results and certain key metrics in 2011, when compared to 2010.

Prior to the closing of this acquisition, we had accounted for our investment in CCE under the equity method of

accounting. Under the equity method of accounting, we recorded our proportionate share of CCE’s net income or loss

53