BB&T 2008 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

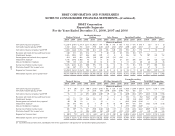

BB&T CORPORATION AND SUBSIDIARIES

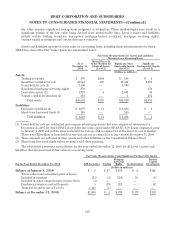

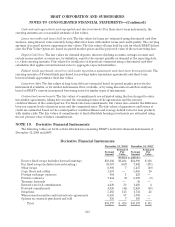

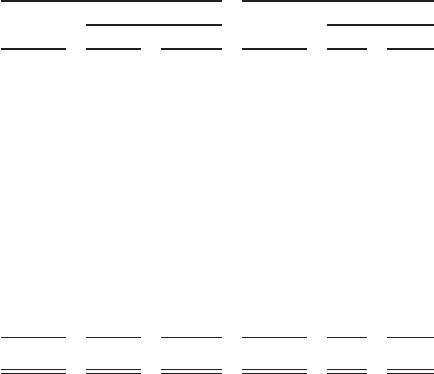

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

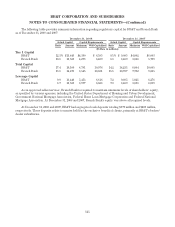

The following tables disclose data with respect to BB&T’s derivative financial instrument classifications and

hedging relationships:

Derivative Classifications and Hedging Relationships

December 31, 2008 December 31, 2007

Notional

Amount

Fair Value Notional

Amount

Fair Value

Gain Loss Gain Loss

(Dollars in millions)

Derivatives Designated as Cash Flow Hedges:

Hedging business loans $ 1,250 $ 45 $ — $ 2,119 $ 20 $ —

Hedging overnight and short-term funding 4,100 6 (31) 1,750 — (14)

Hedging 3 Month LIBOR funding 3,755 6 (39) 2,934 — (8)

Derivatives Designated as Fair Value Hedges:

Hedging long-term debt 4,160 585 — 8,300 148 (6)

Hedging municipal securities 354 — (150) 446 — (33)

Hedging certificates of deposit 357 15 — — — —

Derivatives Designated as Net Investment Hedges:

Hedging foreign exchange 73 — (1) — — —

Derivatives Not Designated as Hedges 60,128 1,066 (876) 31,648 241 (167)

Total $74,177 $1,723 $(1,097) $47,197 $409 $(228)

At December 31, 2008 and 2007, BB&T had designated notional values of $4.9 billion and $8.7 billion,

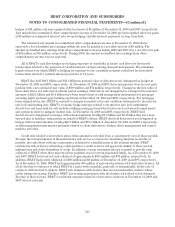

respectively, of derivatives as fair value hedges. At December 31, 2008, fair value hedges reflected a net

unrealized gain of $450 million, with instruments in a gain position reflecting a fair value of $600 million recorded

in other assets and instruments in a loss position with a fair value of $150 million recorded in other liabilities. At

December 31, 2007, derivatives designated as fair value hedges reflected a net unrealized gain of $109 million,

composed of instruments in a gain position with a fair value of $148 million and instruments in a loss position with

a fair value of $39 million. BB&T terminated a fair value hedge related to its long-term debt during the fourth

quarter of 2008 and received proceeds of $266 million. The proceeds from this termination were included in cash

flows from financing activities and the related gain is being amortized over the remaining term of the debt. The

impact on earnings resulting from fair value hedge ineffectiveness was a loss of $10 million during 2008 and a loss

of $2 million during 2007 and 2006, respectively.

At December 31, 2008 and 2007, BB&T had designated derivatives with notional values of $9.1 billion and

$6.8 billion, respectively, as cash flow hedges. These instruments were in a net loss position of $13 million and $2

million at December 31, 2008 and 2007, respectively. The impact on earnings resulting from the ineffectiveness of

cash flow hedges was a loss of $1 million during 2008 and was not material for 2007 and 2006, respectively.

BB&T’s floating rate business loans, Federal funds purchased, institutional certificates of deposit, other time

deposits, medium term bank notes and long term debt expose it to variability in cash flows for interest payments.

The risk management objective for these assets and liabilities is to hedge the variability in the interest payments.

This objective is met by entering into interest rate swaps, and interest rate collars and caps. Interest rate collars

and caps fix the interest payments when interest rates on the hedged item exceed predetermined rates.

Accumulated other comprehensive income included $73 million and $14 million in unrecognized after-tax gains on

interest rate swaps, caps, floors and collars hedging variable interest payments on business loans at December 31,

2008 and 2007, respectively. These amounts included unrecognized after-tax gains on terminated swaps, caps and

collars of $45 million and $7 million at December 31, 2008 and December 31, 2007, respectively. In addition,

accumulated other comprehensive income included $28 million and $14 million in net unrecognized after-tax losses

on interest rate swaps, caps and floors hedging variable interest payments on short-term funding at

December 31, 2008 and 2007, respectively. These amounts included unrecognized after-tax gains on terminated

134