BB&T 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

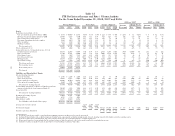

include money rate savings accounts, investor deposit accounts, savings accounts, individual retirement accounts

and other time deposits. Interest checking accounts also increased by $1.4 billion from the prior year and client

certificates of deposit (“CDs”) increased by $965 million. For the year ended December 31, 2008, total deposits

averaged $88.8 billion, an increase of $5.3 billion, or 6.4%, compared to 2007. The increase in average deposits was

primarily the result of a $2.4 billion, or 7.0%, increase in average other client deposits, and a $2.1 billion, or 26.7%,

increase in average other interest-bearing deposits. The overall increase in year-end deposits included the impact

of the acquisition of $506 million in deposits from Haven Trust, which was completed late in the fourth quarter of

2008. The increase in average deposits also included the impact of the acquisition of Coastal which was completed

during 2007.

Average other client deposits represent the largest component of BB&T’s deposits and composed 41.3% of

total average deposits for 2008, compared to 41.0% during 2007. CDs are the second largest source and composed

30.3% of total average deposits for 2008 compared to 31.2% for 2007. The remainder of client deposits consists of

noninterest-bearing deposits and interest-checking accounts, which comprised 17.4% of total average deposits in

the current year, compared to 18.5%, for last year. BB&T also gathers other interest-bearing deposits through

wholesale funding products, which include negotiable certificates of deposit and Eurodollar deposits. Average

other interest-bearing deposits represented 11.0% of total average deposits for 2008, as compared to 9.3% for

2007.

BB&T experienced solid deposit growth during 2008, which accelerated during the second half of the year, as

BB&T gained many new client relationships from competitors. The growth in deposits during 2008 included

strong increases in corporate banking relationships and investor deposit accounts, as BB&T focused its efforts on

these segments. In addition, BB&T was able to achieve growth in client CDs, even as rates declined to historical

lows throughout the year. Average noninterest-bearing deposits declined slightly in 2008, as business clients

continued to minimize their balances in noninterest-bearing accounts. The decline in business noninterest-bearing

balances was offset by growth in balances from consumer clients. The growth in other interest-bearing deposits is

largely driven by the relative cost of these funding sources compared to other short-term and long-term

borrowings.

The average rate paid on interest-bearing deposits dropped to 2.50% during 2008, from 3.73% in 2007. The

average cost for interest-bearing deposits declined during 2008 as management was able to lower rates in

response to the Federal Reserve cutting interest rates. The average rates paid on the various categories of

interest-bearing deposits also decreased as follows: CDs decreased to 3.66% in the current year from 4.61% in

2007; other client deposits decreased to 1.67% in the current year from 2.82% in 2007; interest checking decreased

to 1.19% in 2008 from 2.31% in 2007; and other interest-bearing deposits decreased to 2.71% in 2008 from 5.15% in

2007.

BB&T also uses various types of short-term borrowings in meeting funding needs. While client deposits

remain the primary source for funding loan originations, management uses short-term borrowings as a

supplementary funding source for loan growth and other balance sheet management purposes. Short-term

borrowings comprised 7.7% of total funding needs on average in 2008 as compared to 7.4% in 2007. See Note 9

“Federal Funds Purchased, Securities Sold Under Agreements to Repurchase and Short-Term Borrowed Funds”

in the “Notes to Consolidated Financial Statements” herein for further disclosure. The types of short-term

borrowings used by the Corporation include Federal funds purchased, which comprised 5.4% of total short-term

borrowings, and securities sold under repurchase agreements, which comprised 27.2% of short-term borrowings

at year-end 2008. Master notes, which are short-term borrowings issued to BB&T’s clients, represented 15.8% of

total short-term borrowings at December 31, 2008. U.S. Treasury tax and loan deposit notes, borrowings under

the treasury auction facility and short-term bank notes are also used to meet short-term funding needs and

comprised the remaining 51.6% of these types of funding sources as of December 31, 2008. Short-term borrowings

at the end of 2008 were $10.8 billion, an increase of $154 million, or 1.4% compared to year-end 2007. Average

short-term borrowings totaled $10.6 billion during 2008 compared to $9.3 billion last year, an increase of 13.5%.

The rates paid on average short-term borrowings declined from 4.55% in 2007 to 2.44% during 2008. The decrease

in the cost of short-term borrowings primarily resulted from a lower average Federal funds rate in effect during

2008 compared to 2007. At December 31, 2008, the targeted Federal funds rate was a range of zero percent to

51