BB&T 2008 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

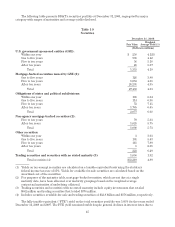

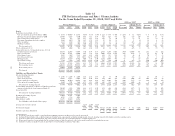

changes in the overall composition of the securities portfolio with a larger concentration of higher-yielding

mortgage-backed and municipal securities. The yield on mortgage-backed securities issued by government-

sponsored entities decreased from 5.15% to 4.94% and the FTE yield on state and municipal securities decreased

from 6.65% last year to 6.33% in the current year, while the yield on U.S. government-sponsored entity securities

increased from 4.53% in 2007 to 4.86% in 2008. The yield on non-agency mortgage-backed securities increased

from 5.78% during 2007 to 5.81% in 2008.

Loans and Leases

BB&T emphasizes commercial lending to small and medium-sized businesses, consumer lending, mortgage

lending and specialized lending with an overall goal of maximizing the profitability of the loan portfolio while

maintaining strong asset quality. The various categories of loan products offered by BB&T are discussed under

“Lending Activities” in the “Overview and Description of Business” section herein. BB&T is a full-service lender

with approximately one-half of its loan portfolio to businesses and one-half to individual consumers. Average

commercial loans, including lease receivables, comprised 50.0% of the loan portfolio during 2008, compared to

48.3% in 2007. Average direct retail loans comprised 16.4% of average loans in 2008, compared to 17.6% in 2007.

Average sales finance loans comprised 6.5% of average loans in 2008, compared to 6.7% in 2007. Average

revolving credit loans comprised 1.7% of average loans in 2008 and 2007. Average mortgage loans comprised

19.5% of average total loans for 2008, compared to 19.9% a year ago. Average loans originated by BB&T’s

specialized lending subsidiaries represented 5.9% of average total loans in 2008 compared to 5.8% in the prior

year.

BB&T’s loan portfolio, excluding loans held for sale, increased $6.3 billion, or 7.0%, compared to year-end

2007. Average total loans and leases for 2008 increased $7.2 billion, or 8.2%, compared to 2007. The growth in the

loan portfolio was primarily a result of strong internal growth in the commercial and industrial lending portfolio,

as well as growth in the mortgage and specialized lending portfolios. The growth in average loans during 2008,

includes the impact of the acquisition of Coastal Financial Corporation (“Coastal”), which was acquired during

2007.

Average commercial loans and leases increased $5.1 billion, or 12.0%, in 2008 as compared to 2007. Overall,

the commercial loan and lease portfolio showed strong growth during 2008. The mix of the commercial loan

portfolio has shifted somewhat, as commercial real estate lending has slowed due to a slower real estate market

and management’s efforts to reduce exposure to the real estate market. This has been offset by an increased focus

on commercial and industrial loans. BB&T experienced stronger trends in the fourth quarter of 2008 both in

commercial and industrial lending and income producing commercial real estate lending primarily due to

challenges facing many in-market competitors that has allowed BB&T to attract new clients.

The pace of growth in the direct retail loan portfolio slowed further in 2008, due to a difficult residential real

estate market, which decreased demand for home equity loan products. Sales finance loans and revolving credit

reflected solid growth rates of 5.3% and 14.0%, respectively, during 2008. BB&T concentrates its efforts on the

highest quality borrowers in both of these product markets. Sales finance loans were negatively affected by weak

auto sales; however BB&T has been gaining market share in this portfolio as many competitors have withdrawn

from indirect automobile lending in our footprint.

Average mortgage loans increased $1.1 billion, or 6.2%, compared to 2007. Management views mortgage

loans as an integral part of BB&T’s relationship-based credit culture. BB&T is a large originator of residential

mortgage loans, with 2008 originations of $16.4 billion. The vast majority of mortgage loans originated during

2008 were conforming mortgage loans that were either sold in the secondary market or held in the loans held for

sale portfolio at year-end. Loans held for sale, which is almost entirely comprised of government-conforming

mortgage loans increased 82.8% compared to year-end 2007 as refinance activity significantly increased late in the

fourth quarter due to the historically low loan rates for mortgages. At December 31, 2008, BB&T was servicing

$40.7 billion in residential mortgages owned by third parties and $19.0 billion of mortgage loans owned by BB&T,

including $18.4 billion classified as mortgage loans and $573 million classified as securities available for sale.

Average loans originated by BB&T’s specialized lending subsidiaries increased $445 million, or 8.6%,

compared to 2007. The growth in the specialized lending portfolio was driven by strong internal loan growth in

46