BB&T 2008 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

|

|

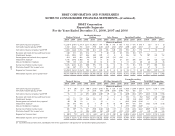

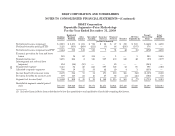

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

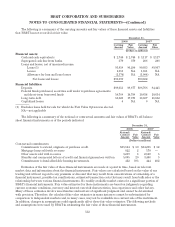

for employee incentives, certain revenues of Residential Mortgage Banking, Sales Finance, Specialized Lending,

Insurance Services, Financial Services and other segments are reflected in the individual segment results and

also allocated to the Banking Network. This double counting of revenue is reflected in intersegment net referral

fees and eliminated to arrive at consolidated results. Allocation methodologies are subject to periodic adjustment

as the internal management accounting system is revised and business or product lines within the segments

change. Also, because the development and application of these methodologies is a dynamic process, the financial

results presented may be periodically revised.

BB&T’s overall objective is to maximize shareholder value by optimizing return on equity and managing

risk. Allocations of capital and the economic provision for loan and lease losses are designed to address this

objective. Capital is assigned to each segment on an economic basis, using management’s assessment of the

inherent risks associated with the segment. Capital allocations are made to cover the following risk categories:

credit risk, liquidity risk, interest rate risk, option risk, basis risk, market risk and operational risk. Each

segment is evaluated based on a risk-adjusted return on capital. Capital assignments are not equivalent to

regulatory capital guidelines, and the total amount assigned to all segments typically varies from total

consolidated shareholders’ equity.

The economic provision for loan and lease losses is also allocated to the relevant segments based on

management’s assessment of the segments’ risks as described above. Unlike the provision for loan and lease

losses recorded pursuant to generally accepted accounting principles, the economic provision adjusts for the

impact of expected credit losses over the effective lives of the related loans and leases. Any over or under

allocated provision for loan and lease losses is reflected in Parent/Reconciling Items to arrive at consolidated

results.

BB&T allocates expenses to the reportable segments based on various methodologies, including volume and

amount of loans and deposits and the number of full-time equivalent employees. A portion of corporate overhead

expense is not allocated, but is retained in corporate accounts and reflected as Parent/Reconciling Items in the

accompanying tables. Income taxes are allocated to the various segments based on taxable income and statutory

rates applicable to the segment.

BB&T utilizes a funds transfer pricing (“FTP”) system to eliminate the effect of interest rate risk from the

segments’ net interest income because such risk is centrally managed within the Treasury segment. The FTP

system credits or charges the segments with the economic value or cost of the funds the segments create or use.

The FTP system provides a funds credit for sources of funds and a funds charge for the use of funds by each

segment. The net FTP credit or charge, which includes intercompany interest income and expense, is reflected as

net funds transfer pricing in the accompanying tables.

Early in 2009, management evaluated its allocation methodologies for the economic provision for loan and

lease losses and FTP given the deterioration in the loan portfolio and the dislocation in the LIBOR rate during

2008. Based on this evaluation, management updated its allocations of the economic provision for loan and lease

losses and FTP to reflect these events that occurred in 2008. The 2008 results presented in the three-year

comparative table reflect the updated methodologies for the economic provision for loan and lease losses and

FTP. In addition, a separate presentation of the 2008 results based on the prior methodologies has been provided.

Banking Network

BB&T’s Banking Network serves individual and business clients by offering a variety of loan and deposit

products and other financial services. The Banking Network is primarily responsible for serving client

relationships, and, therefore, is credited with revenue from the Residential Mortgage Banking, Financial

Services, Insurance Services, Specialized Lending, Sales Finance and other segments, which is reflected in net

referral fees. Amortization and depreciation expense that has been allocated to the segment totaled $82 million,

$86 million and $88 million for 2008, 2007 and 2006, respectively.

137