BB&T 2008 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

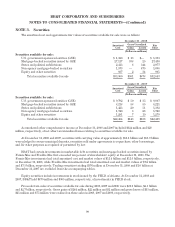

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging

Activities—an amendment of SFAS No. 133,” (“SFAS No. 161”). SFAS No. 161 requires that an entity provide

enhanced disclosures related to derivative and hedging activities. SFAS No. 161 is effective for BB&T on

January 1, 2009.

In April 2008, the FASB issued FSP FAS 142-3, “Determination of the Useful Life of Intangible

Assets” (“FSP FAS 142-3”). FSP FAS 142-3 amends the factors an entity should consider in developing renewal

or extension assumptions used in determining the useful life of recognized intangible assets under FASB SFAS

No. 142, “Goodwill and Other Intangible Assets” (“SFAS No. 142”). The intent of FSP FAS 142-3 is to improve

the consistency between the useful life of a recognized intangible asset under SFAS No. 142 and the period of

expected cash flows used to measure the fair value of the asset under SFAS No. 141(R). FSP FAS 142-3 is

effective for BB&T on January 1, 2009, and applies prospectively to intangible assets that are acquired

individually or with a group of other assets in business combinations and asset acquisitions. The adoption of FSP

FAS 142-3 was not material to the consolidated financial statements.

In December 2008, the FASB issued FSP FAS 140-4 and FIN 46(R)-8, “Disclosures by Public Entities

(Enterprises) about Transfers of Financial Assets and Interests in Variable Interest Entities,” (“FSP FAS 140-4

and FIN 46(R)-8”). The disclosures required by FSP FAS 140-4 and FIN 46(R)-8 are intended to provide greater

transparency to financial statement users about a transferor’s continuing involvement with transferred financial

assets and an enterprise’s involvement with variable interest entities and qualifying SPEs. The disclosures

required by FSP FAS 140-4 and FIN 46(R)-8 are included in Note 8 and Note 15 to these consolidated financial

statements.

In December 2008, the FASB issued FSP FAS 132(R)-1, “Employers’ Disclosures about Postretirement

Benefit Plan Assets,” (“FSP FAS 132(R)-1”). The objectives of FSP FAS 132(R)-1 are to provide users of the

financial statements with more detailed information related to the major categories of plan assets, the inputs and

valuation techniques used to measure the fair value of plan assets and the effect of fair value measurements using

significant unobservable inputs (Level 3) on changes in plan assets for the period, as well as how investment

allocation decisions are made, including the factors that are pertinent to an understanding of investment policies

and strategies. The disclosures about plan assets required by FSP FAS 132(R)-1 are effective for BB&T on

December 31, 2009.

In January 2009, the FASB issued FSP EITF 99-20-01, “Amendments to the Impairment Guidance of EITF

Issue No. 99-20,” (“FSP EITF 99-20-01”). The objective of FSP EITF 99-20-01 is to achieve more consistency in

the determination of whether an other-than-temporary impairment has occurred. FSP EITF 99-20-01 also retains

and emphasizes the objective of an other-than-temporary impairment assessment and the related disclosure

requirements in FASB Statement No. 115, “Accounting for Certain Investments in Debt and Equity Securities”,

and other related guidance. The adoption of FSP EITF 99-20-01, which was effective for BB&T on December 31,

2008, was not material to the consolidated financial statements.

NOTE 2. Business Combinations

Financial Institution Acquisitions

On December 12, 2008, BB&T announced the acquisition of all the deposits and $61 million in assets of Haven

Trust Bank of Duluth, Georgia through an agreement with the Federal Deposit Insurance Corporation (“FDIC”).

Haven Trust Bank operated four branches with approximately $506 million in deposits.

On May 1, 2007, BB&T completed the acquisition of Coastal Financial Corporation (“Coastal”), a $1.7 billion

bank holding company headquartered in Myrtle Beach, South Carolina. In conjunction with this transaction,

BB&T issued approximately 8.8 million shares of common stock and 574 thousand stock options valued in the

aggregate at $400 million. Including subsequent adjustments, BB&T recorded $246 million in goodwill and $47

million in amortizing intangibles, which are primarily core deposit intangibles.

97