BB&T 2008 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

automobile lending, as many competitors exited this business during 2008. Additionally, healthy growth trends

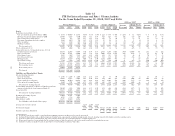

were evident in premium finance and equipment finance during the fourth quarter.

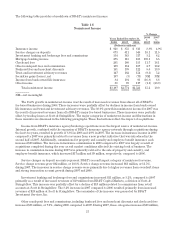

The average annualized FTE yield for 2008 for the total loan portfolio was 6.35% compared to 7.67% for the

prior year. The 132 basis point decrease in the average yield on loans resulted primarily from the repricing of

variable rate loans and maturing loans with higher yields that were replaced with lower-yielding loans and leases.

The prime rate, which is the basis for pricing many commercial and consumer loans, declined 400 basis points

during 2008 to 3.25% at year-end as the Federal Reserve Board lowered rates seven times during 2008 in

response to the economic recession, challenges in the residential real estate markets, and disruptions in other

financial markets. The average prime rate in effect during 2008 and 2007 was 5.09% and 8.05%, respectively.

Asset Quality and Credit Risk Management

BB&T has established the following general practices to manage credit risk:

Šlimiting the amount of credit that individual lenders may extend;

Šestablishing a process for credit approval accountability;

Šcareful initial underwriting and analysis of borrower, transaction, market and collateral risks;

Šongoing servicing of individual loans and lending relationships;

Šcontinuous monitoring of the portfolio, market dynamics and the economy; and

Šperiodically reevaluating the bank’s strategy and overall exposure as economic, market and other

relevant conditions change.

BB&T’s lending strategy, which focuses on relationship-based lending within our markets and smaller

individual loan balances, continues to produce credit quality that is better than its peer group of financial

institutions. As measured by relative levels of nonperforming assets and net charge-offs, BB&T’s asset quality

has remained significantly better than published industry averages.

47