BB&T 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

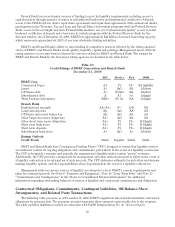

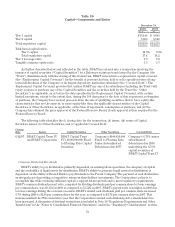

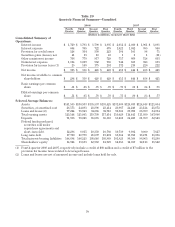

Table 26

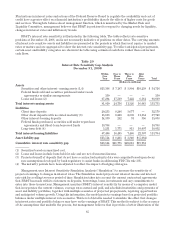

Capital—Components and Ratios

December 31,

2008 2007

(Dollars in millions)

Tier 1 capital $13,446 $ 9,085

Tier 2 capital 5,663 5,148

Total regulatory capital $19,109 $14,233

Risk-based capital ratios:

Tier 1 capital 12.3% 9.1%

Total regulatory capital 17.4 14.2

Tier 1 leverage ratio 9.9 7.2

Tangible common equity ratio 5.3 5.7

As further described below and reflected in the table, BB&T has entered into a transaction involving the

issuance of capital securities (“Capital Securities”) by a Delaware statutory trust formed by the Company (the

“Trust”). Simultaneously with the closing of this transaction, BB&T entered into a replacement capital covenant

(the “Replacement Capital Covenant”) for the benefit of persons that buy, hold or sell a specified series of long-

term indebtedness of the Company or its largest depository institution subsidiary (the “Covered Debt”). The

Replacement Capital Covenant provides that neither BB&T nor any of its subsidiaries (including the Trust) will

repay, redeem or purchase any of the Capital Securities and the securities held by the Trust (the “Other

Securities”), as applicable, on or before the date specified in the Replacement Capital Covenant, with certain

limited exceptions, except to the extent that, during the 180 days prior to the date of that repayment, redemption

or purchase, the Company has received proceeds from the sale of qualifying securities that (i) have equity-like

characteristics that are the same as, or more equity-like than, the applicable characteristics of the Capital

Securities or Other Securities, as applicable, at the time of repayment, redemption or purchase, and (ii) the

Company has obtained the prior approval of the Federal Reserve Board, if such approval is then required by the

Federal Reserve Board.

The following table identifies the (i) closing date for the transaction, (ii) issuer, (iii) series of Capital

Securities issued, (iv) Other Securities, and (v) applicable Covered Debt.

Closing

Date Issuer Capital Securities Other Securities Covered Debt

6/12/07 BB&T Capital Trust IV

and BB&T Corporation

BB&T Capital Trust

IV’s $600,000,000 Fixed

to Floating Rate Capital

Securities

Company’s $600,010,000

Fixed to Floating Rate

Junior Subordinated

Debentures due 2077

Company’s 6.75% junior

subordinated

debentures due 2036

underlying the 6.75%

capital securities of

BB&T Capital Trust II

Common Stock and Dividends

BB&T’s ability to pay dividends is primarily dependent on earnings from operations, the adequacy of capital

and the availability of liquid assets for distribution. BB&T’s ability to generate liquid assets for distribution is

dependent on the ability of Branch Bank to pay dividends to the Parent Company. The payment of cash dividends is

an integral part of providing a competitive return on shareholders’ investments. The Corporation’s policy is to

accomplish this while retaining sufficient capital to support future growth and to meet regulatory requirements.

BB&T’s common dividend payout ratio, computed by dividing dividends paid per common share by basic earnings

per common share, was 68.13% in 2008 as compared to 55.52% in 2007. BB&T’s payout ratio was higher in 2008 due

to lower earnings during the economic recession. BB&T’s annual cash dividends paid per common share increased

5.7% during 2008 to $1.86 per common share for the year, as compared to $1.76 per common share in 2007. This

increase marked the 37th consecutive year that the Corporation’s annual cash dividend paid to shareholders has

been increased. A discussion of dividend restrictions is included in Note 16 “Regulatory Requirements and Other

Restrictions” in the “Notes to Consolidated Financial Statements” and in the “Regulatory Considerations” section.

72