BB&T 2008 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Pension and Postretirement Benefit Obligations

BB&T offers various pension plans and postretirement benefit plans to employees. The calculation of the

obligations and related expenses under these plans requires the use of actuarial valuation methods and

assumptions. Actuarial valuations and assumptions used in the determination of future values of plan assets and

liabilities are subject to management judgment and may differ significantly if different assumptions are used. The

discount rate assumption used to measure the postretirement benefit obligations is set by reference to published

high-quality bond indices, as well as certain hypothetical spot-rate yield curves. These yield curves were

constructed from the underlying bond price and yield data collected as of the plan’s measurement date and are

represented by a series of annualized, individual discount rates with durations ranging from six months to thirty

years. Each discount rate in the curve was derived from an equal weighting of the double A or higher bond

universe, apportioned into distinct maturity groups. For durations where no bond maturities were available, the

discount rates for these maturities were extrapolated based on historical relationships from observable data in

similar markets. These indices and hypothetical curves give only an indication of the appropriate discount rate

because the cash flows of the bonds comprising the indices and curves do not match the projected benefit

payment stream of the plan precisely. For this reason, we also consider the individual characteristics of the plan,

such as projected cash flow patterns and payment durations, when setting the discount rate. Please refer to Note

14 “Benefit Plans” in the “Notes to Consolidated Financial Statements” for disclosures related to BB&T’s benefit

plans, including quantitative disclosures reflecting the impact that changes in certain assumptions would have on

service and interest costs and benefit obligations.

Income Taxes

The calculation of BB&T’s income tax provision is complex and requires the use of estimates and judgments.

As part of the Company’s analysis and implementation of business strategies, consideration is given to the tax

laws and regulations that apply to the specific facts and circumstances for any tax position under evaluation. For

tax positions that are uncertain in nature, management determines whether the tax position is more likely than

not to be sustained upon examination. For tax positions that meet this threshold, management then estimates the

amount of the tax benefit to recognize in the financial statements. Management closely monitors tax

developments in order to evaluate the effect they may have on the Company’s overall tax position and the

estimates and judgments used in determining the income tax provision and records adjustments as necessary.

Analysis of Financial Condition

A summary of the more significant fluctuations in balance sheet accounts is presented below.

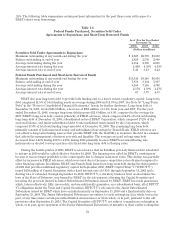

For the year ended December 31, 2008, BB&T’s average assets totaled $136.9 billion, an increase of $10.5

billion, or 8.3%, compared to the 2007 average of $126.4 billion, primarily reflecting growth in average loans and

leases and investment securities. Average loans and leases for 2008 were up $7.2 billion, or 8.2%, from 2007 and

average investment securities increased $1.2 billion, or 5.1%, compared to 2007. The growth in average loans and

leases was led by growth in average commercial loans and leases, which increased $5.1 billion, or 12.0%; average

mortgage loans, which increased $1.1 billion, or 6.2%; and growth in average loans originated by BB&T’s

specialized lending subsidiaries, which increased $445 million, or 8.6%. Total earning assets averaged $120.9

billion in 2008, an increase of $8.5 billion, or 7.6%, compared to 2007. These averages and growth rates include the

effects of acquisitions.

BB&T’s average deposits totaled $88.8 billion, reflecting growth of $5.3 billion, or 6.4%, compared to 2007.

The categories of deposits with the highest growth rates were other interest-bearing deposits, which increased

$2.1 billion, or 26.7%, and other client deposits, which increased $2.4 billion, or 7.0%.

Short-term borrowings include Federal funds purchased, securities sold under repurchase agreements,

master notes, short-term bank notes, treasury tax and loan deposit notes payable and other short-term

borrowings. Average short-term borrowings totaled $10.6 billion for the year ended December 31, 2008, an

increase of $1.3 billion, or 13.5%, from the 2007 average. BB&T also has used long-term debt for a significant

portion of its funding needs. Long-term debt includes Federal Home Loan Bank (“FHLB”) advances, other

secured borrowings by Branch Bank, capital securities issued by unconsolidated trusts and senior and

subordinated debt issued by the Corporation and Branch Bank. Average long-term debt totaled $19.8 billion for

the year ended December 31, 2008, up $1.8 billion, or 9.9%, compared to 2007.

42