BB&T 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

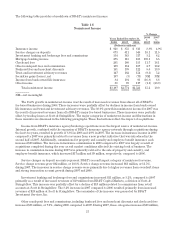

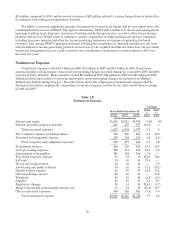

Mortgage banking income increased $160 million, or 139.1% during 2008. BB&T adopted SFAS No. 159, “The

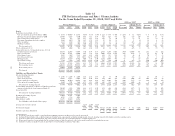

Fair Value Option for Financial Assets and Financial Liabilities-Including an amendment of FASB Statement

No. 115,” (“SFAS No. 159” or the “Fair Value Option”) for the majority of loans originated for sale after

January 1, 2008, and implemented the provisions of Staff Accounting Bulletin No. 109 “Written Loan

Commitments Recorded at Fair Value through Earnings” (“SAB 109’). As a result of the adoption of both

standards, mortgage banking income increased approximately $74 million compared to 2007. Of the $74 million

increase relating to the adoption of these accounting standards, approximately $55 million relates to the

elimination of the provisions of SFAS No. 91 “Accounting for Nonrefundable Fees and Costs Associated with

Originating or Acquiring Loans and Initial Direct Costs of Leases—an amendment of FASB Statements No. 13,

60, and 65 and a rescission of FASB Statement No. 17,” (“SFAS No. 91”) on loans accounted for at fair value and

resulted in a corresponding increase in personnel expense. The net change in the valuation of mortgage servicing

rights resulted in a $38 million increase compared to 2007. The $38 million increase was the result of the mortgage

servicing rights hedge outperforming the decline in the value of the asset. The positive hedge performance was

attributable to (i) the strong appreciation of option-based hedge instruments, which occurs during periods of

extreme interest rate volatility, and (ii) the favorable hedge effectiveness against the interest rate basis

movements between mortgages and swap-based hedge instruments. Excluding the impact of these items,

mortgage banking income increased $48 million, or 43.2%, compared to the prior year. The growth in mortgage

banking income includes strong production revenues from both residential and commercial mortgage banking

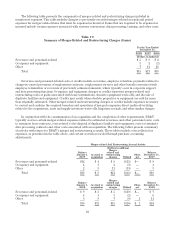

operations. The growth in commercial mortgage banking revenues was the result of the acquisition of Collateral

Real Estate Capital, LLC (“Collateral”) in the fourth quarter of 2007. BB&T combined the operations of

Collateral with its existing mortgage banking operations and renamed the subsidiary Grandbridge Real Estate

Capital LLC (“Grandbridge”). The acquisition of Collateral significantly expanded the size and product offerings

of BB&T’s commercial mortgage banking activities. Mortgage banking income increased $7 million, or 6.5%,

during 2007. The growth in 2007 included an increase of $4 million, or 11.1%, in commercial mortgage banking

income primarily generated by Grandbridge. The acquisition of Collateral in the fourth quarter of 2007 was the

primary reason for the 125.4% increase in commercial mortgage loans serviced for others at year-end 2007

compared to the prior year-end. BB&T’s residential mortgage banking income also increased $3 million during

2007 compared to 2006. While residential mortgage loan sales increased 42.9% during 2007, gains and other

revenues associated with those sales only increased 2.2% due to increased competition in the marketplace.

BB&T recognized $107 million in net securities gains during 2008 compared to net losses of $3 million and $73

million during 2007 and 2006, respectively. The net securities gains recognized in 2008 included $211 million of

gains from securities sales and $104 million of losses as a result of other-than-temporary impairments. The losses

recognized in 2006 were primarily in connection with an announced restructuring of a portion of the securities

portfolio that was undertaken in the fourth quarter of 2006.

Income from bank owned life insurance (“BOLI”) decreased $17 million, or 16.8%, in 2008 compared to 2007,

primarily due to a valuation adjustment that resulted from a decline in the underlying assets of certain insurance

policies. BOLI income increased $8 million, or 8.6%, in 2007 compared to 2006.

Other income decreased slightly in 2008 compared to 2007. The current year included gains related to BB&T’s

ownership interest and sale of Visa, Inc. stock that amounted to $80 million. In addition, revenues from client

derivative activities were $22 million higher in 2008 compared to 2007. These increases were offset by a number of

factors, including a $50 million decline in the value of various financial assets isolated for the purpose of providing

post-employment benefits. The decline in the value of these assets is neutral to net income as these losses relate

to participant’s accounts and reduce the amount of benefits that will be paid in the future. Earnings from

investments in low income housing partnerships that generate tax benefits declined $39 million and net revenues

from BB&T’s venture capital investments declined $26 million. In addition, the current year’s results were

affected by certain items that were recorded in 2007, including the sale of an insurance operation and losses from

capital markets activities as mentioned below. The 23.9%, or $28 million, decrease in 2007 compared to 2006, was

primarily due to approximately $33 million in losses from capital markets activities during the last half of 2007.

These losses were primarily caused by disruptions in the financial markets that decreased the value of certain

trading securities and derivative contracts. In addition, BB&T sold an insurance operation during 2007, which

produced a gain of $19 million. BB&T also generated $17 million in additional revenues from client derivative

activities. Other income for 2007 also reflects lower revenues from venture capital investments, which decreased

59