BB&T 2008 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

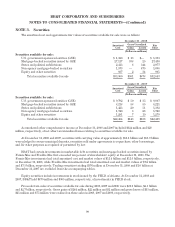

In October 2008, the FASB issued FASB Staff Position (“FSP”) FSP FAS 157-3, “Determining the Fair

Value of a Financial Asset When the Market for That Asset Is Not Active,” (“FSP FAS 157-3”). FSP FAS 157-3

clarifies the application of SFAS No. 157 in determining the fair value of a financial asset during periods of

inactive markets. FSP FAS 157-3 was effective as of September 30, 2008 and did not have a material impact on

the consolidated financial statements.

In September 2006, the FASB reached a consensus on Emerging Issues Task Force (“EITF”) Issue 06-4,

“Accounting for Deferred Compensation and Postretirement Benefit Aspects of Endorsement Split-Dollar Life

Insurance Arrangements,” (“EITF Issue 06-4”). In March 2007, the FASB reached a consensus on EITF Issue

06-10, “Accounting for Collateral Assignment Split-Dollar Life Insurance Arrangements,” (“EITF Issue 06-10”).

Both of these standards require a company to recognize an obligation over an employee’s service period based

upon the substantive agreement with an employee such as the promise to maintain a life insurance policy or

provide a death benefit. BB&T adopted the provisions of these standards effective January 1, 2008. The adoption

of these EITF issues was not material to the consolidated financial statements.

In February 2007, the FASB issued SFAS No. 159, which permits companies to choose to measure many

financial instruments and certain other items at fair value, on an instrument-by-instrument basis. Once a

company has elected to record eligible items at fair value, the decision is generally irrevocable. The objective of

SFAS No. 159 is to improve financial reporting by providing companies with the opportunity to mitigate

volatility in reported earnings caused by measuring related assets and liabilities differently without having to

apply complex hedge accounting provisions. BB&T adopted SFAS No. 159 effective January 1, 2008, and elected

the fair value option for certain loans held for sale originated on or after January 1, 2008. The adoption of SFAS

No. 159 was not material to the consolidated financial statements.

In November 2007, the SEC Staff issued Staff Accounting Bulletin No. 109 (“SAB No. 109”) “Written Loan

Commitments Recorded at Fair Value through Earnings”, which supersedes the guidance previously issued in

SAB No. 105 “Application of Accounting Principles to Loan Commitments” (“SAB No. 105”). SAB No. 109

expresses the current view of the Staff that the expected net future cash flows related to the associated servicing

of the loan should be included in the measurement of all written loan commitments that are accounted for at fair

value through earnings. The provisions of SAB No. 109 affect only the timing of mortgage banking income

recognition and are effective for loan commitments entered into on or after January 1, 2008. The adoption of the

provisions of SAB No. 109 was not material to BB&T’s consolidated financial statements.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations,” (“SFAS

No. 141(R)”). SFAS No. 141(R) requires the acquiring entity in a business combination to recognize the full fair

value of assets acquired and liabilities assumed in the transaction (whether a full or partial acquisition);

establishes the acquisition-date fair value as the measurement objective for all assets acquired and liabilities

assumed; requires expensing of most transaction and restructuring costs; and requires the acquirer to disclose to

investors and other users all of the information needed to evaluate and understand the nature and financial effect

of the business combination. SFAS No. 141(R) is effective for BB&T for business combinations entered into on or

after January 1, 2009.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial

Statements—an amendment of ARB No. 51,” (“SFAS No. 160”). SFAS No. 160 requires that a noncontrolling

interest in a subsidiary be accounted for as equity in the consolidated statement of financial position and that net

income include the amounts for both the parent and the noncontrolling interest, with a separate amount

presented in the income statement for the noncontrolling interest share of net income. SFAS No. 160 also

expands the disclosure requirements and provides guidance on how to account for changes in the ownership

interest of a subsidiary. SFAS No. 160 is effective prospectively for BB&T on January 1, 2009, except for the

presentation and disclosure provisions which will be applied retrospectively for all periods presented. As of

December 31, 2008 and 2007, BB&T had $44 million and $32 million, respectively of liabilities related to minority

interest that will be reclassed to shareholders’ equity upon adoption of SFAS No. 160. In addition, BB&T

recorded $10 million, $12 million and $5 million of expense related to its minority interest during the years ended

December 31, 2008, 2007 and 2006, respectively.

96