BB&T 2008 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

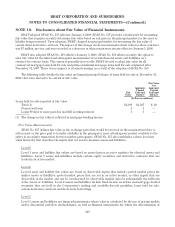

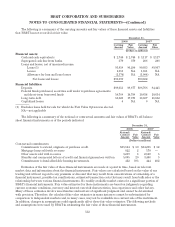

hedges of $11 million and unrecognized after-tax losses of $3 million at December 31, 2008 and 2007, respectively.

Also included in accumulated other comprehensive income at December 31, 2008 are unrecognized after-tax gains

of $3 million on terminated interest rate swaps hedging variable interest payments on long term debt.

The estimated net amount in accumulated other comprehensive income at December 31, 2008 that is

expected to be reclassified into earnings within the next 12 months is a net after-tax loss of $9 million. The

amount reclassified into earnings from other comprehensive income during 2008 and 2007 was a net after-tax gain

of $61 million and $5 million, respectively. During 2006, the amount reclassified into earnings from other

comprehensive income was not material.

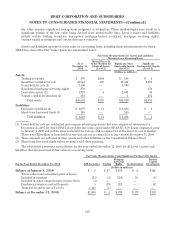

All of BB&T’s cash flow hedges are hedging exposure to variability in future cash flows for forecasted

transactions related to the payment of variable interest on then existing financial instruments. The maximum

length of time over which BB&T is hedging its exposure to the variability in future cash flows for forecasted

transactions related to variable interest payments is 7.4 years.

BB&T also held $60.1 billion and $31.6 billion in notional value of derivatives not designated as hedges at

December 31, 2008 and 2007, respectively. At December 31, 2008 and 2007, these instruments were in a net gain

position with a net estimated fair value of $190 million and $74 million, respectively. Changes in the fair value of

these derivatives are reflected in current period earnings. Derivatives not designated as a hedge in the notional

amounts of $25.1 billion and $9.4 billion have been entered into as risk management instruments for mortgage

servicing rights and mortgage banking operations at December 31, 2008 and 2007, respectively. For mortgage

loans originated for sale, BB&T is exposed to changes in market rates and conditions subsequent to the interest

rate lock and funding date. BB&T’s economic hedge strategy related to its interest rate lock commitment

derivatives and loans held for sale includes utilizing mortgage-based derivatives such as forward commitments

and options in order to mitigate market risk. At December 31, 2008 and 2007, respectively, BB&T held

derivatives not designated as hedges with notional amounts totaling $9.3 billion and $6.4 billion that have been

entered into to facilitate transactions on behalf of BB&T’s clients. BB&T also held derivatives not designated as

hedges with notional amounts totaling $25.7 billion and $15.8 billion at December 31, 2008 and 2007, respectively,

as risk management instruments primarily related to client derivatives, balance sheet management and capital

markets activities.

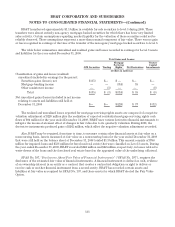

Credit risk related to derivatives arises when amounts receivable from a counterparty exceed those payable.

Because the notional amount of the instruments only serves as a basis for calculating amounts receivable or

payable, the risk of loss with any counterparty is limited to a small fraction of the notional amount. BB&T

controls the risk of loss by subjecting counterparties to credit reviews and approvals similar to those used in

making loans and other extensions of credit. In addition, certain counterparties are required to provide cash

collateral to BB&T when their unsecured loss positions exceed certain negotiated limits. As of December 31, 2008

and 2007, BB&T had received cash collateral of approximately $165 million and $75 million, respectively. In

addition, BB&T had posted collateral of $180 million and $8 million at December 31, 2008 and 2007, respectively.

As of December 31, 2008, BB&T had approximately $59 million of unsecured positions with derivative dealers. All

of the derivative contracts to which BB&T is a party settle monthly, quarterly or semiannually. In the case of

contracts with derivative dealers, BB&T only transacts with dealers that are national market makers whose

credit ratings are strong. Further, BB&T has netting agreements with the dealers with which it does business.

Because of these factors, BB&T’s credit risk exposure related to derivatives contracts at December 31, 2008 and

2007 was not material.

135