BB&T 2008 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2008 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

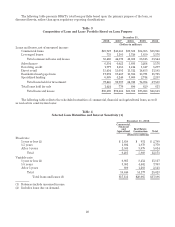

|

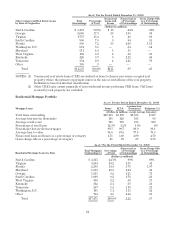

(Dollars

in millions)

(3) The above table excludes:

(i) consumer loans $12,018

(ii) real estate mortgage loans 46,772

(iii) loans held for sale 1,424

(iv) lease receivables 2,007

Total $62,221

Scheduled repayments are reported in the maturity category in which the payment is due. Determinations of

maturities are based upon contract terms. BB&T’s credit policy typically does not permit automatic renewal of

loans. At the scheduled maturity date (including balloon payment date), the customer generally must request a

new loan to replace the matured loan and execute either a new note or note modification with rate, terms and

conditions negotiated at that time.

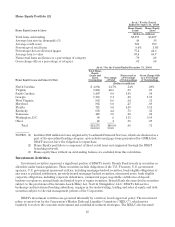

Allowance for Loan and Lease Losses and Reserve for Unfunded Lending Commitments

The allowance for loan and lease losses is determined based on management’s best estimate of probable

losses that are inherent in the portfolio at the balance sheet date. BB&T’s allowance is driven by existing

conditions and observations, and reflects losses already incurred, even if not yet identifiable.

The Corporation determines the allowance based on an ongoing evaluation of the loan and lease portfolios.

This evaluation is inherently subjective because it requires material estimates, including the amounts and timing

of cash flows expected to be received on impaired loans. Those estimates may be susceptible to significant change.

Increases to the allowance are made by charges to the provision for credit losses, which is reflected in the

Consolidated Statements of Income. Loans or leases deemed to be uncollectible are charged against the

allowance. Recoveries of previously charged-off amounts are credited to the allowance.

In addition to the allowance for loan and lease losses, BB&T also estimates probable losses related to binding

unfunded lending commitments. The methodology to determine such losses is inherently similar to the

methodology used in calculating the allowance for commercial loans, adjusted for factors specific to binding

commitments, including the probability of funding and exposure at funding. The reserve for unfunded lending

commitments is included in accounts payable and other liabilities on the Consolidated Balance Sheets. Changes to

the reserve for unfunded lending commitments are made by charges or credits to the provision for credit losses.

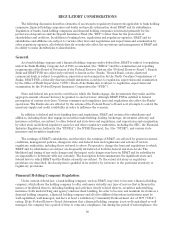

Reserve Policy and Methodology

The allowance for loan and lease losses consists of (1) a component for individual loan impairment recognized

and measured pursuant to Statement of Financial Accounting Standards (“SFAS”) No. 114, “Accounting by

Creditors for Impairment of a Loan,” and (2) components of collective loan impairment recognized pursuant to

SFAS No. 5, “Accounting for Contingencies,” including a component that is unallocated. BB&T maintains specific

reserves for individually impaired loans pursuant to SFAS No. 114. A loan is impaired when, based on current

information and events, it is probable that BB&T will be unable to collect all amounts due (interest as well as

principal) according to the contractual terms of the loan agreement. On a quarterly basis, BB&T reviews all

commercial lending relationships with outstanding debt of $2 million or more that have been classified as

substandard or doubtful. Loans are considered impaired when the borrower does not have the cash flow capacity

or willingness to service the debt according to contractual terms, or it does not appear reasonable to assume that

the borrower will continue to pay according to the contractual agreement. The amount of impairment is based on

the present value of expected cash flows discounted at the loan’s effective interest rate, and/or the value of

collateral adjusted for any origination costs and nonrefundable fees that existed at the time of origination.

Reserves established pursuant to the provisions of SFAS No. 5 for collective impairment reflect an estimate

of losses inherent in the loan and lease portfolios as of the balance sheet reporting date. Embedded loss estimates

are based on current migration rates and current risk mix. Embedded loss estimates may be adjusted to reflect

current economic conditions and current portfolio trends including credit quality, concentrations, aging of the

portfolio, and significant policy and underwriting changes. In the commercial lending portfolio, each loan is

21