Coca Cola 2015 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2015 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

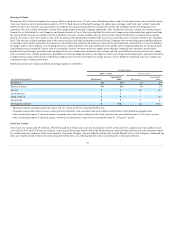

appropriate amount of taxable income the Company should report in the United States in connection with its licensing of intangible property to certain

related foreign licensees regarding the manufacturing, distribution, sale, marketing and promotion of products in overseas markets. The IRS designated the

matter for litigation on October 15, 2015. The Company firmly believes that the IRS' claims are without merit and plans to pursue all available administrative

and judicial remedies necessary to resolve this matter. To that end, the Company filed a petition in U.S. Tax Court on December 14, 2015. The Company

believes that the final adjudication of this matter will not have a material impact on its consolidated financial position, results of operations or cash flows and

that it has adequate tax reserves for all tax matters. However, if this dispute were to be ultimately determined adversely to us, the additional tax, interest and

any potential penalties could have a material adverse impact on the Company's financial position, results of operations or cash flows. Refer to Note 11 of

Notes to Consolidated Financial Statements for additional information.

A number of years may elapse before a particular matter for which we have established a reserve is audited and finally resolved. The number of years with

open tax audits varies depending on the tax jurisdiction. The tax benefit that has been previously reserved because of a failure to meet the "more likely than

not" recognition threshold would be recognized in our income tax expense in the first interim period when the uncertainty disappears under any one of the

following conditions: (1) the tax position is "more likely than not" to be sustained, (2) the tax position, amount, and/or timing is ultimately settled through

negotiation or litigation, or (3) the statute of limitations for the tax position has expired. Settlement of any particular issue would usually require the use of

cash.

Tax law requires items to be included in the tax return at different times than when these items are reflected in the consolidated financial statements. As a

result, the annual tax rate reflected in our consolidated financial statements is different from that reported in our tax return (our cash tax rate). Some of these

differences are permanent, such as expenses that are not deductible in our tax return, and some differences reverse over time, such as depreciation expense.

These timing differences create deferred tax assets and liabilities. Deferred tax assets and liabilities are determined based on temporary differences between

the financial reporting and tax bases of assets and liabilities. The tax rates used to determine deferred tax assets or liabilities are the enacted tax rates in effect

for the year and manner in which the differences are expected to reverse. Based on the evaluation of all available information, the Company recognizes future

tax benefits, such as net operating loss carryforwards, to the extent that realizing these benefits is considered more likely than not.

We evaluate our ability to realize the tax benefits associated with deferred tax assets by analyzing our forecasted taxable income using both historical and

projected future operating results; the reversal of existing taxable temporary differences; taxable income in prior carryback years (if permitted); and the

availability of tax planning strategies. A valuation allowance is required to be established unless management determines that it is more likely than not that

the Company will ultimately realize the tax benefit associated with a deferred tax asset. As of December 31, 2015, the Company's valuation allowances on

deferred tax assets were $477 million and primarily related to uncertainties regarding the future realization of recorded tax benefits on tax loss carryforwards

generated in various jurisdictions. Current evidence does not suggest we will realize sufficient taxable income of the appropriate character within the

carryforward period to allow us to realize these deferred tax benefits. If we were to identify and implement tax planning strategies to recover these deferred tax

assets or generate sufficient income of the appropriate character in these jurisdictions in the future, it could lead to the reversal of these valuation allowances

and a reduction of income tax expense. The Company believes it will generate sufficient future taxable income to realize the tax benefits related to the

remaining net deferred tax assets in our consolidated balance sheets.

The Company does not record a U.S. deferred tax liability for the excess of the book basis over the tax basis of its investments in foreign corporations to the

extent that the basis difference results from earnings that meet the indefinite reversal criteria. These criteria are met if the foreign subsidiary has invested, or

will invest, the undistributed earnings indefinitely. The decision as to the amount of undistributed earnings that the Company intends to maintain in non-

U.S. subsidiaries takes into account items including, but not limited to, forecasts and budgets of financial needs of cash for working capital, liquidity plans,

capital improvement programs, merger and acquisition plans, and planned loans to other non-U.S. subsidiaries. The Company also evaluates its expected

cash requirements in the United States. Other factors that can influence that determination are local restrictions on remittances (for example, in some countries

a central bank application and approval are required in order for the Company's local country subsidiary to pay a dividend), economic stability and asset risk.

As of December 31, 2015, undistributed earnings of the Company's foreign subsidiaries that met the indefinite reversal criteria amounted to $31.9 billion.

Refer to Note 14 of Notes to Consolidated Financial Statements.

The Company's effective tax rate is expected to be 22.5 percent in 2016. This estimated tax rate does not reflect the impact of any unusual or special items

that may affect our tax rate in 2016.

44