Coca Cola 2015 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2015 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

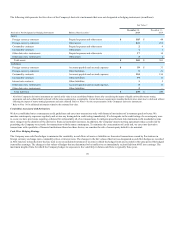

|

|

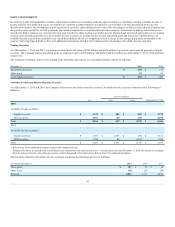

Each CBA generally has a term of 10 years and is renewable, in most cases by the bottler and in some cases by the Company, indefinitely for successive

additional terms of 10 years each. Under the CBA, the bottlers will make ongoing quarterly payments to the Company based on their gross profit in the

refranchised territories throughout the term of the CBA, including renewals, in exchange for the grant of the exclusive territory rights.

Contemporaneously with the grant of these rights, the Company sold the distribution assets, certain working capital items, and the exclusive rights to

distribute certain beverage brands not owned by the Company, but distributed by CCR, in each of these territories to the respective bottlers in exchange for

cash. These rights include, where applicable, the recently acquired Monster distribution rights discussed above. During the years ended December 31, 2015

and December 31, 2014, cash proceeds from these sales totaled $362 million and $143 million, respectively. Included in the cash proceeds for the years

ended December 31, 2015 and December 31, 2014 was $83 million and $42 million, respectively, from Coca-Cola Bottling Co. Consolidated, an equity

method investee. Under the applicable accounting guidance, we were required to derecognize all of the tangible assets sold as well as the intangible assets

transferred, including distribution rights, customer relationships and an allocated portion of goodwill related to these territories.

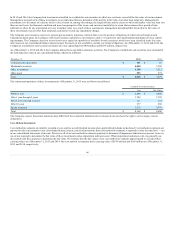

Additionally, in September 2015, the Company announced the formation of a new National Product Supply System ("NPSS") which will facilitate optimal

operation of the U.S. product supply system. Under the NPSS, the Company and several of its existing independent producing bottlers will administer key

national product supply activities for these bottlers, which currently represent approximately 95 percent of the U.S. produced volume. As part of the NPSS, it

is anticipated that each of these bottlers will acquire certain production facilities from CCR in exchange for cash, subject to the parties reaching definitive

agreements. The transition of these production facilities is anticipated to take place by the end of 2017.

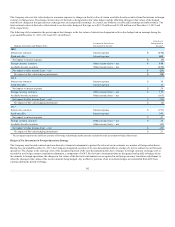

We recognized noncash losses of $1,006 million and $799 million during the years ended December 31, 2015 and December 31, 2014, respectively. These

losses primarily related to the derecognition of the intangible assets transferred or reclassified as held for sale, and were included in the line item other income

(loss) — net in our consolidated statements of income. See further discussion of assets and liabilities held for sale below. We expect to recover the value of

the intangible assets transferred to the bottlers under the CBAs through the future quarterly payments; however, as the payments for the territory rights are

dependent on the bottlers' future gross profit in these territories, they are considered a form of contingent consideration.

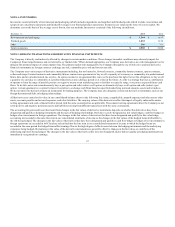

There is diversity in practice as it relates to the accounting for contingent consideration by the seller. The seller can account for the future contingent

payments received as a gain contingency, recognizing the amounts in the income statement only after the related contingencies are resolved and the gain is

realized, which in this arrangement will be quarterly as the bottlers earn gross profit in the transferred territories. Alternatively, the seller can record a

receivable for the contingent consideration at fair value on the date of sale and record any future differences between the payments received and this

receivable in the income statement as they occur. We elected the gain contingency treatment since the quarterly payments will be received throughout the

terms of the CBAs, including all subsequent renewals, regardless of the cumulative amount received as compared to the value of the intangible assets

transferred.

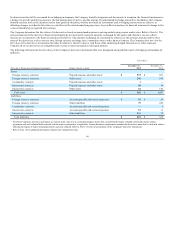

Philippine Bottling Operations

On January 25, 2013, the Company sold a 51 percent interest in our Philippine bottling operations to Coca-Cola FEMSA, an equity method investee. The

Company accounts for our remaining 49 percent ownership interest in the Philippine bottling operations under the equity method of accounting. As a result

of this transaction, we remeasured our remaining investment in the Philippine bottling operations to fair value taking into consideration the sale price of the

majority ownership interest. Coca-Cola FEMSA has an option to purchase our remaining ownership interest in the Philippine bottling operations at any time

during the seven years following closing based on the initial purchase price plus a defined return. Coca-Cola FEMSA also has an option exercisable during

the sixth year after closing to sell its ownership interest back to the Company at a price not to exceed the initial purchase price.

92