Coca Cola 2015 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2015 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

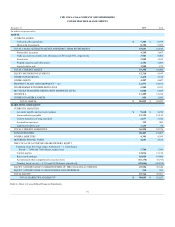

Income Taxes

Income tax expense includes United States, state, local and international income taxes, plus a provision for U.S. taxes on undistributed earnings of foreign

subsidiaries not deemed to be indefinitely reinvested. Deferred tax assets and liabilities are recognized for the tax consequences of temporary differences

between the financial reporting basis and the tax basis of existing assets and liabilities. The tax rate used to determine the deferred tax assets and liabilities is

the enacted tax rate for the year and manner in which the differences are expected to reverse. Valuation allowances are recorded to reduce deferred tax assets

to the amount that will more likely than not be realized. The Company records taxes that are collected from customers and remitted to governmental

authorities on a net basis in our consolidated statements of income.

The Company is involved in various tax matters, with respect to some of which the outcome is uncertain. We establish reserves to remove some or all of the

tax benefit of any of our tax positions at the time we determine that it becomes uncertain based upon one of the following conditions: (1) the tax position is

not "more likely than not" to be sustained, (2) the tax position is "more likely than not" to be sustained, but for a lesser amount, or (3) the tax position is

"more likely than not" to be sustained, but not in the financial period in which the tax position was originally taken. For purposes of evaluating whether or

not a tax position is uncertain, (1) we presume the tax position will be examined by the relevant taxing authority that has full knowledge of all relevant

information; (2) the technical merits of a tax position are derived from authorities such as legislation and statutes, legislative intent, regulations, rulings and

case law and their applicability to the facts and circumstances of the tax position; and (3) each tax position is evaluated without consideration of the

possibility of offset or aggregation with other tax positions taken. A number of years may elapse before a particular uncertain tax position is audited and

finally resolved or when a tax assessment is raised. The number of years subject to tax assessments varies depending on the tax jurisdiction. The tax benefit

that has been previously reserved because of a failure to meet the "more likely than not" recognition threshold would be recognized in our income tax

expense in the first interim period when the uncertainty disappears under any one of the following conditions: (1) the tax position is "more likely than not" to

be sustained, (2) the tax position, amount, and/or timing is ultimately settled through negotiation or litigation, or (3) the statute of limitations for the tax

position has expired. Refer to Note 11 and Note 14.

Translation and Remeasurement

We translate the assets and liabilities of our foreign subsidiaries from their respective functional currencies to U.S. dollars at the appropriate spot rates as of

the balance sheet date. Generally, our foreign subsidiaries use the local currency as their functional currency. Changes in the carrying value of these assets

and liabilities attributable to fluctuations in spot rates are recognized in foreign currency translation adjustment, a component of AOCI. Refer to Note 15.

Income statement accounts are translated using the monthly average exchange rates during the year.

Monetary assets and liabilities denominated in a currency that is different from a reporting entity's functional currency must first be remeasured from the

applicable currency to the legal entity's functional currency. The effect of this remeasurement process is recognized in the line item other income (loss) — net

in our consolidated statements of income and is partially offset by the impact of our economic hedging program for certain exposures on our consolidated

balance sheets. Refer to Note 5.

Hyperinflationary Economies

A hyperinflationary economy is one that has cumulative inflation of 100 percent or more over a three-year period. In accordance with U.S. GAAP, local

subsidiaries in hyperinflationary economies are required to use the U.S. dollar as their functional currency and remeasure the monetary assets and liabilities

not denominated in U.S. dollars using the rate applicable to conversion of a currency for purposes of dividend remittances. All exchange gains and losses

resulting from remeasurement are recognized currently in income.

Venezuela has been designated as a hyperinflationary economy. In February 2013, the Venezuelan government devalued its currency to an official rate of

exchange ("official rate") of 6.3 bolivars per U.S. dollar. At that time, the Company remeasured the net monetary assets of our Venezuelan subsidiary at the

official rate. As a result of the devaluation, we recognized a loss of $140 million from remeasurement in the line item other income (loss) — net in our

consolidated statement of income.

Beginning in the first quarter of 2014, the Venezuelan government recognized three legal exchange rates to convert bolivars to the U.S. dollar: (1) the official

rate of 6.3 bolivars per U.S. dollar; (2) SICAD 1, which was available to foreign investments and designated industry sectors to exchange a limited volume of

bolivars for U.S. dollars using a bid rate established at weekly auctions; and (3) SICAD 2, which applied to transactions that did not qualify for either the

official rate or SICAD 1. As of March 28, 2014, the three legal exchange rates were 6.3 (official rate), 10.8 (SICAD 1) and 50.9 (SICAD 2). We determined that

the SICAD 1 rate was the most appropriate rate to use for remeasurement given our circumstances and estimates of the applicable rate at which future

transactions could be settled, including the payment of dividends. Therefore, as of March 28, 2014, we remeasured the net monetary assets of our Venezuelan

subsidiary using an exchange rate of 10.8 bolivars per U.S.

87