Electronic Arts 2012 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2012 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

Annual Report

Item 7A: Quantitative and Qualitative Disclosures About Market Risk

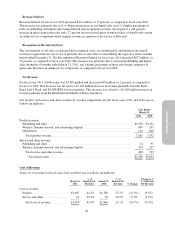

MARKET RISK

We are exposed to various market risks, including changes in foreign currency exchange rates, interest rates and

market prices, which have experienced significant volatility in light of the global economic downturn. Market

risk is the potential loss arising from changes in market rates and market prices. We employ established policies

and practices to manage these risks. Foreign currency option and forward contracts are used to hedge anticipated

exposures or mitigate some existing exposures subject to foreign exchange risk as discussed below. While we do

not hedge our short-term investment portfolio, we protect our short-term investment portfolio against different

market risks, including interest rate risk as discussed below. Our cash and cash equivalents portfolio consists of

highly liquid investments with insignificant interest rate risk and original or remaining maturities of three months

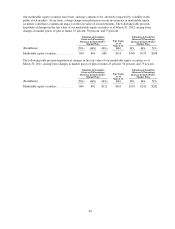

or less at the time of purchase. We also do not currently hedge our market price risk relating to our marketable

equity securities and we do not enter into derivatives or other financial instruments for trading or speculative

purposes.

Foreign Currency Exchange Rate Risk

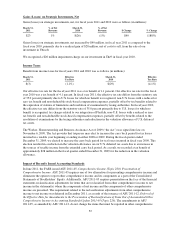

Cash Flow Hedging Activities. From time to time, we hedge a portion of our foreign currency risk related to

forecasted foreign-currency-denominated sales and expense transactions by purchasing foreign currency option

contracts that generally have maturities of 15 months or less. These transactions are designated and qualify as

cash flow hedges. The derivative assets associated with our hedging activities are recorded at fair value in other

current assets on our Consolidated Balance Sheets. The effective portion of gains or losses resulting from

changes in the fair value of these hedges is initially reported, net of tax, as a component of accumulated other

comprehensive income in stockholders’ equity. The gross amount of the effective portion of gains or losses

resulting from changes in the fair value of these hedges is subsequently reclassified into net revenue or research

and development expenses, as appropriate, in the period when the forecasted transaction is recognized in our

Consolidated Statements of Operations. In the event that the gains or losses in accumulated other comprehensive

income are deemed to be ineffective, the ineffective portion of gains or losses resulting from changes in fair

value, if any, is reclassified to interest and other income (expense), net, in our Consolidated Statements of

Operations. In the event that the underlying forecasted transactions do not occur, or it becomes remote that they

will occur, within the defined hedge period, the gains or losses on the related cash flow hedges are reclassified

from accumulated other comprehensive income to interest and other income (expense), net, in our Consolidated

Statements of Operations. During the reporting periods, all forecasted transactions occurred and, therefore, there

were no such gains or losses reclassified into interest and other income (expense), net. Our hedging programs are

designed to reduce, but do not entirely eliminate, the impact of currency exchange rate movements in net revenue

and research and development expenses. As of March 31, 2012, we had foreign currency option contracts to

purchase approximately $74 million in foreign currency and to sell approximately $78 million of foreign

currency. All of the foreign currency option contracts outstanding as of March 31, 2012 will mature in the next

12 months. As of March 31, 2011, we had foreign currency option contracts to purchase approximately $40

million in foreign currency and to sell approximately $10 million of foreign currencies. As of March 31, 2012,

these foreign currency option contracts outstanding had a total fair value of $2 million and are included in other

current assets. As of March 31, 2011, the fair value of these outstanding foreign currency option contracts was

immaterial and are included in other current assets.

Balance Sheet Hedging Activities. We use foreign currency forward contracts to mitigate foreign currency risk

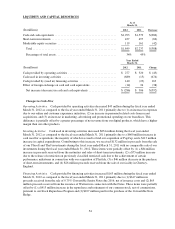

associated with foreign-currency-denominated monetary assets and liabilities, primarily intercompany

receivables and payables. The foreign currency forward contracts generally have a contractual term of three

months or less and are transacted near month-end. Our foreign currency forward contracts are not designated as

hedging instruments, and are accounted for as derivatives whereby the fair value of the contracts is reported as

other current assets or accrued and other current liabilities on our Consolidated Balance Sheets, and gains and

losses resulting from changes in the fair value are reported in interest and other income (expense), net, in our

Consolidated Statements of Operations. The gains and losses on these foreign currency forward contracts

generally offset the gains and losses on the underlying foreign-currency-denominated monetary assets and

liabilities, which are also reported in interest and other income (expense), net, in our Consolidated Statements of

59