Electronic Arts 2012 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2012 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

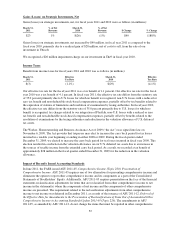

Operations. In certain cases, the amount of such gains and losses will significantly differ from the amount of

gains and losses recognized on the underlying foreign-currency-denominated monetary asset or liability, in which

case our results will be impacted. As of March 31, 2012, we had foreign currency forward contracts to purchase

and sell approximately $242 million in foreign currencies. Of this amount, $197 million represented contracts to

sell foreign currencies in exchange for U.S. dollars, $37 million to purchase foreign currency in exchange for

U.S. dollars, and $8 million to sell foreign currency in exchange for British pound sterling. As of March 31,

2011, we had foreign currency forward contracts to purchase and sell approximately $187 million in foreign

currencies. Of this amount, $140 million represented contracts to sell foreign currencies in exchange for U.S.

dollars, $31 million to purchase foreign currency in exchange for U.S. dollars and $16 million to sell foreign

currency in exchange for British pound sterling. The fair value of our foreign currency forward contracts was

immaterial as of March 31, 2012 and 2011.

We believe the counterparties to these foreign currency forward and option contracts are creditworthy

multinational commercial banks. While we believe the risk of counterparty nonperformance is not material, the

disruption in the global financial markets has impacted some of the financial institutions with which we do

business. Further, the continued sovereign debt crisis in Europe could lead to increased counterparty risk with

respect to financial institutions and other business partners, who are particularly vulnerable to the instability in

certain European markets. A sustained decline in the financial stability of financial institutions as a result of the

disruption in the financial markets could affect our ability to secure credit-worthy counterparties for our foreign

currency hedging programs.

Notwithstanding our efforts to mitigate some foreign currency exchange rate risks, there can be no assurance that

our hedging activities will adequately protect us against the risks associated with foreign currency fluctuations.

As of March 31, 2012, a hypothetical adverse foreign currency exchange rate movement of 10 percent or 15

percent would have resulted in potential declines in the fair value of the premiums on our foreign currency option

contracts used in cash flow hedging of less than $2 million in each scenario. As of March 31, 2012, a

hypothetical adverse foreign currency exchange rate movement of 10 percent or 15 percent would have resulted

in potential losses on our foreign currency forward contracts used in balance sheet hedging of $24 million and

$37 million, respectively. This sensitivity analysis assumes a parallel adverse shift of all foreign currency

exchange rates against the U.S. dollar; however, all foreign currency exchange rates do not always move in such

manner and actual results may differ materially.

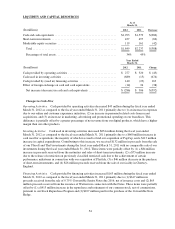

Interest Rate Risk

Our exposure to market risk for changes in interest rates relates primarily to our short-term investment portfolio.

We manage our interest rate risk by maintaining an investment portfolio generally consisting of debt instruments

of high credit quality and relatively short maturities. However, because short-term investments mature relatively

quickly and are required to be reinvested at the then-current market rates, interest income on a portfolio

consisting of short-term investments is more subject to market fluctuations than a portfolio of longer term

investments. Additionally, the contractual terms of the investments do not permit the issuer to call, prepay or

otherwise settle the investments at prices less than the stated par value. Our investments are held for purposes

other than trading. Also, we do not use derivative financial instruments in our short-term investment portfolio.

60