Electronic Arts 2012 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2012 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

Annual Report

Impact of Recently Issued Accounting Standards

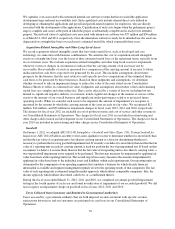

In June 2011, the FASB issued ASU 2011-05, Comprehensive Income (Topic 220):Presentation of Comprehensive

Income. ASU 2011-05 requires one of two alternatives for presenting comprehensive income and eliminates the option

to report other comprehensive income and its components as a part of the Consolidated Statements of Stockholders’

Equity. Additionally, ASU 2011-05 requires presentation on the face of the financial statements reclassification

adjustments for items that are reclassified from other comprehensive income to net income in the statement(s) where

the components of net income and the components of other comprehensive income are presented. The requirement

related to the reclassification adjustments from other comprehensive income to net income was deferred in December

2011, as a result of the issuance of ASU 2011-12, Deferral of the Effective Date for Amendments to the Presentation of

Reclassifications of Items Out of Accumulated Other Comprehensive Income in Accounting Standards Update 2011-05

(Topic 220). The amendments in ASU 2011-05, as amended by ASU 2011-12, do not change the items that must be

reported in other comprehensive income or when an item of other comprehensive income must be reclassified to net

income. ASU 2011-05, as amended by ASU 2011-12 is effective for fiscal years and interim periods within those years

beginning after December 15, 2011 and is to be applied retrospectively. We will adopt ASU 2011-05 during the first

quarter of fiscal year 2013. We do not expect the adoption of ASU 2011-05, as amended by ASU 2011-12 to have a

material impact on our Consolidated Financial Statements.

In December 2011, the FASB issued ASU 2011-11, Disclosures about Offsetting Assets and Liabilities, which

creates new disclosure requirements about the nature of an entity’s rights of offset and related arrangements

associated with its financial instruments and derivative instruments. The disclosure requirements are effective for

annual reporting periods beginning on or after January 1, 2013, and interim periods therein, with retrospective

application required. The new disclosures are designed to make financial statements that are prepared under U.S.

Generally Accepted Accounting Principles more comparable to those prepared under International Financial

Reporting Standards. We are evaluating the impact of ASU 2011-11 on our Consolidated Financial Statements.

(2) FAIR VALUE MEASUREMENTS

Fair value is the price that would be received from selling an asset or paid to transfer a liability in an orderly

transaction between market participants at the measurement date. When determining fair value, we consider the

principal or most advantageous market in which we would transact and consider assumptions that market

participants would use when pricing the asset or liability. We measure certain financial and nonfinancial assets

and liabilities at fair value on a recurring and nonrecurring basis.

Fair Value Hierarchy

The three levels of inputs that may be used to measure fair value are as follows:

•Level 1. Quoted prices in active markets for identical assets or liabilities.

•Level 2. Observable inputs other than quoted prices included within Level 1, such as quoted prices for

similar assets or liabilities, quoted prices in markets with insufficient volume or infrequent transactions

(less active markets), or model-derived valuations in which all significant inputs are observable or can be

derived principally from or corroborated with observable market data for substantially the full term of the

assets or liabilities.

•Level 3. Unobservable inputs to the valuation methodology that are significant to the measurement of the

fair value of assets or liabilities.

On January 1, 2012, we adopted the FASB Accounting Standards Update (“ASU”) 2011-04, Fair Value

Measurement (Topic 820): Amendments to Achieve Common Fair Value Measurement and Disclosure

Requirements in U.S. GAAP and IFRSs. The guidance limits the highest-and-best-use measure to nonfinancial

assets, permits certain financial assets and liabilities with offsetting positions in market or counterparty credit

risks to be measured at a net basis, and provides guidance on the applicability of premiums and

discounts. Additionally, the guidance expands the disclosures on Level 3 inputs by requiring quantitative

disclosure of the unobservable inputs and assumptions, as well as description of the valuation processes and the

sensitivity of the fair value to changes in unobservable inputs. Adoption of this new guidance did not have a

material impact on our Consolidated Financial Statements.

75