General Motors 2011 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2011 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

salaried pension plan and to 6.5% for the hourly pension plan. The resulting weighted-average return is 6.2%. The overall decrease is

primarily due to a different asset mix consisting of a higher proportion of fixed income investments compared to last year. The

salaried pension plan has a higher target proportion of fixed income investments than the hourly pension plan and therefore, a lower

expected return on assets than the hourly pension plan.

Another key assumption in determining net pension expense is the assumed discount rate to be used to discount plan obligations.

We estimate this rate for U.S. plans using a cash flow matching approach, which uses projected cash flows matched to spot rates along

a high quality corporate yield curve to determine the present value of cash flows to calculate a single equivalent discount rate.

Significant differences in actual experience or significant changes in assumptions may materially affect the pension obligations.

The effect of actual results differing from assumptions and the changing of assumptions are included in unamortized net actuarial

gains and losses that are subject to amortization to expense over future periods.

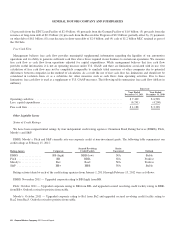

The following table summarizes the unamortized actuarial gain (loss) (before tax) on pension plans (dollars in billions):

Successor

December 31, 2011 December 31, 2010

Unamortized actuarial gain (loss) ................................................... $(3.8) $2.9

The following table illustrates the sensitivity to a change in certain assumptions for the pension plans, holding all other assumptions

constant (dollars in millions):

Successor

U.S. Plans Non-U.S. Plans

Effect on 2012

Pension

Expense

Effect on

December 31,

2011

PBO

Effect on 2012

Pension

Expense

Effect on

December 31,

2011

PBO

25 basis point decrease in discount rate .............................. !$130 +$2,730 +$45 +$ 774

25 basis point increase in discount rate .............................. +$110 !$2,660 !$6 !$ 735

25 basis point decrease in expected return on assets .................... +$210 N/A +$34 N/A

25 basis point increase in expected return on assets .................... !$210 N/A !$34 N/A

The following data illustrates the sensitivity of changes in pension expense and pension obligation based on the last remeasurement

of the U.S hourly pension plan at December 31, 2011 (dollars in millions):

Successor

Change in future benefit units

Effect on

2012

Pension Expense

Effect on

December 31, 2011

PBO

One percentage point increase in benefit units .......................................... +$101 +$308

One percentage point decrease in benefit units .......................................... !$ 98 !$299

Refer to Note 18 to our consolidated financial statements for the weighted-average expected long-term rate of return on plan assets,

weighted-average discount rate on plan obligations, actual and expected return on plan assets, and for a discussion of the inputs used

to determine fair value for each significant asset class or category.

Other Postretirement Benefits

OPEB plans are accounted for on an actuarial basis, which requires the selection of various assumptions, including a discount rate

and healthcare cost trend rates. In the U.S. Old GM established a discount rate assumption to reflect the yield of a hypothetical

portfolio of high quality, fixed-income debt instruments that would produce cash flows sufficient in timing and amount to satisfy

projected future benefits.

General Motors Company 2011 Annual Report 57