Philips 2006 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2006 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

Philips Annual Report 2006 11

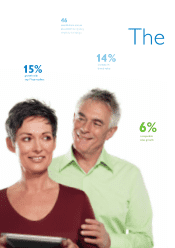

our brand value gaining 14% to an estimated USD 6.7

billion, moving us into the top 50 global brands as ranked

by leading brand consultant Interbrand.

Set up a separate legal structure for Semiconductors

and create value by pursuing strategic options

This goal was achieved in full thanks to a tremendous

effort by all concerned – a true case of speed and

teamwork. Not only did we set up a separate legal

structure for Semiconductors in a record nine months,

we also completed an exhaustive review of the strategic

options available. This led to the sale, in September, of

a majority stake in the business to a private equity

consortium. Valuing our Semiconductors division at

EUR 8.3 billion, I believe the deal represents good

business for Philips.

Increase the number of entrepreneurial business leaders

with broad-based experience

It is vital that our future leaders have a broad base of

experience across multiple aspects of Philips’ businesses.

I am glad to say that of all the top potentials who move

to another position, now some two-thirds are moving to

another business or functional area, a signifi cant increase

compared to previous years.

Our acquisitions of relatively young, fast-growing small

and medium-sized enterprises also make an important

contribution in bringing new entrepreneurial business

leaders into the company, with some of them being

promoted to more senior positions within Philips.

Over the past two years we have conducted an objective

assessment and benchmark program among our senior

executives to ensure we have the right people in the

right places and – via our talent pool – effective succession

planning. Our leadership programs place heavy emphasis

on business development, e.g. in emerging markets or our

Incubators, which are an ideal environment for the

development of entrepreneurial talent.

Accelerate movement to become a simpler,

market-oriented organization

During 2006 we took a number of important steps to

further simplify Philips and base our actions on true

customer and market insights.

First of all, we extended our approach to organize

ourselves around our customers in professional

healthcare,

professional lighting and consumer retail.

We expanded our international key account management

in retail from our top 7 accounts to our top 20. This top

20 represents 18% of our total sales, and in 2006 showed

12% sales growth compared to 2005. We also deployed

this successful approach deeper into the organization.

Under the leadership of the International Retail Board,

every country now has a set of key national accounts

on which divisions work together to ensure a simpler

customer experience and higher sales.

Furthermore, we took out a complete regional

management layer, reducing the distance between our

global businesses and their local markets. On a country

level, we integrated country management with local

marketing and sales management.

In 2007 we will see our key account system evolve to its

next stage. In our top 20 national markets the consumer

activities will further align their consumer retail approach

in a collaborative model; in all other, mostly smaller markets,

the consumer activities’ sales forces will be integrated. This

will make our combined Philips footprint in local markets

stronger and more professional, so that we are easier and

more attractive for our customers to deal with.

In 2006 we rolled out the next wave of our “sense and

simplicity” brand campaign, highlighting the benefi ts offered

by simplicity, as well as allowing customers to directly

experience simplicity fi rst hand by means of experiential

marketing. These brand investments are paying off, with

“Going forward, we will build upon the growth and value creation

momentum we have developed over the past few years.”

54 The Philips sectors 86 Risk management 100 Report of the Supervisory Board 110 Financial Statements