Philips 2006 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2006 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

Philips Annual Report 2006 95

as back-up for short-term fi nancing requirements that

would normally be satisfi ed through the Commercial

Paper Program and EUR 9,524 million of investments

in its main available-for-sale securities, trading securities

and listed equity-accounted investees at market value

per December 31, 2006. The Company has a lock-up

period associated with the sale of shares in TPV that

expires in September 2008. Furthermore, the LG.Philips

LCD shareholders agreement with LG Electronics, states

that both companies will maintain a holding of at least

30% each until July 2007.

Equity price risk

Philips is a shareholder in several publicly listed companies

such as TSMC, LG.Philips LCD, TPV and JDS Uniphase.

As a result, Philips is exposed to potential fi nancial loss

through movements in the share prices of these companies.

The aggregate equity price exposure of these investments

amounted to approximately EUR 9,524 million at year-

end 2006 (2005: EUR 11,252 million including shares that

were sold during 2006). Philips also holds options on the

shares of TPV through a convertible bond issued to Philips

in September 2005, the face value of the bond being the

USD equivalent of EUR 160 million and the value of the

option at year-end EUR 40 million. Philips does not hold

derivatives in its own stock, or in the above-mentioned

listed companies except for the embedded derivatives

in the convertible bond as mentioned.

Commodity price risk

Philips is a purchaser of certain base metals, precious

metals and energy. Philips hedges certain commodity price

risks using derivative instruments to minimize signifi cant,

unanticipated earnings fl uctuations caused by commodity

price volatility. The commodity price derivatives that

Philips enters into are concluded as cash fl ow hedges

to offset forecasted purchases. A 10% increase in the

market price of all commodities would increase the

fair value of the derivatives by EUR 2 million.

Credit risk

Credit risk represents the loss that would be recognized

at the reporting date if counterparties failed completely

to perform their payment obligations as contracted.

Credit risk is present within the trade receivables

of Philips. To reduce exposure to credit risk, Philips

performs ongoing credit evaluations of the fi nancial

condition of its customers and adjusts payment terms

and credit limits when appropriate.

Philips invests available cash and cash equivalents with

various fi nancial institutions and is exposed to credit risk

with these counterparties. Philips is also exposed to credit

risks in the event of non-performance by counterparties

with respect to fi nancial derivative instruments.

Philips actively manages concentration risk and on a daily

basis measures the potential loss under certain stress

scenarios, should a fi nancial counterparty default. These

worst-case scenario losses are monitored and limited

by the company. As of December 31, 2006 the company

had credit risk exceeding EUR 25 million to the following

number of counterparties:

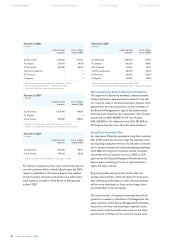

Credit risk with number of counterparties

25-100

million

100-500

million

500-1,500

million

AAA-rated bank counter-

parties 1 − 1

AAA-rated money market

funds 2 − −

AA-rated bank counterparties 2 6 2

A-rated bank counterparties 1 − −

Non-rated money market

funds − 1 −

Lower-rated bank counter-

parties in China 2 − −

The company does not enter into any fi nancial derivative

instruments to protect against default by fi nancial

counterparties. However, where possible the company

requires all fi nancial counterparties with whom it deals

in derivative transactions to complete legally enforceable

netting agreements under an International Swap Dealers

Association master agreement or otherwise prior to

trading and, whenever possible, to have a strong credit

rating from Standard & Poor’s and Moody’s Investor

Services. Wherever possible, cash is invested and fi nancial

transactions are concluded with fi nancial institutions

with strong credit ratings.

Country risk

Philips is exposed to country risk by the very nature

of running a global business. Country risk is the risk

that political, legal, or economic developments in a single

country could adversely impact our performance. The

country risk per country is defi ned as the sum of equity

of all subsidiaries and associated companies in country

cross-border transactions, such as intercompany loans,

54 The Philips sectors 86 Risk management 100 Report of the Supervisory Board 110 Financial Statements