Philips 2006 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2006 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

Philips Annual Report 2006190

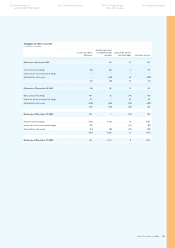

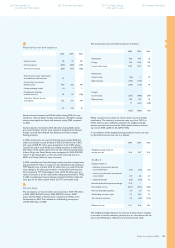

Reconciliation from IFRS to US GAAP

The Company provides for transparency purposes for the users of the fi nancial statements, the following

reconciliations from IFRS to US GAAP.

Reconciliation of net income from IFRS to US GAAP

in millions of euros

2004 2005 2006

Net income as per the consolidated

statements of income on an IFRS basis 2,783 3,374 4,664

Adjustments to reconcile to US GAAP:

Reversal of capitalized product

development cost

-

(216 ) (263 ) (271 )

Reversal of amortization of product

development costs

-

167 197 213

Reversal of additional net pensions

and other charges

-

128 97 292

Financial income and expense - 182 (5 ) −

Adjustment of results of equity-

accounted investees

-

(34 ) (521 ) (18 )

Provisions - − − (65 )

Income tax effect on IFRS adjustments - (46 ) (24 ) 22

Discontinued operations - (101 ) (5 ) 472

Other - (27 ) 18 74

Net income as per the

consolidated statements of income

on a US GAAP basis 2,836 2,868 5,383

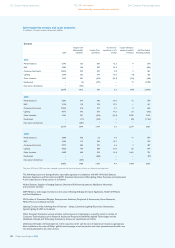

The major differences between IFRS and US GAAP that affect stockholders’ equity and net income are the following:

IFRS requires capitalization and subsequent amortization of development cost if the relevant conditions for

capitalization are met, whereas development cost under US GAAP is recorded as an expense.

Standards for pension accounting are signifi cantly different between US GAAP and IFRS. Prepaid pension assets

under IFRS can only be recognized to the extent that economic benefi ts are available in the form of refunds from

the plan or reductions in future contributions to the plan. Further, parts of the funded status remain unrecognized

under IFRS, while SFAS No. 158 requires full recognition of the funded status.

Under IFRS, goodwill is not amortized as from 2004. Since goodwill was no longer amortized as from 2002 under

US GAAP, IFRS has two additional years of goodwill amortization. This is also a reason for differences in equity-

accounted investees under IFRS and US GAAP.

IFRS requires up-front profi t recognition of operational sale-and-leaseback transactions when the sale is at market

conditions, whereas US GAAP requires amortization.

Different accounting policies for valuation and discounting give rise to a reconciliation item for provisions.

The differences as explained above affect income taxes and therefore deferred income taxes.

The composition of equity under IFRS is affected by the exemption

of IFRS 1 that allows the inclusion of the existing

negative cumulative

translation differences of EUR 3.4 billion in retained earnings as per January 1, 2004. As a result

of the application of this exemption, the recycling of translation gains and losses from equity to the income

statement differs when comparing US GAAP and IFRS. For 2005 and 2006, this mainly affects the results from

equity-accounted investees and discontinued operations respectively.

•

•

•

•

•

•

•

Reconciliation of stockholders’ equity from IFRS to US GAAP

in millions of euros

Dec. 31,

2005

Dec. 31,

2006

Stockholders’ equity as per the consolidated

balance sheets on an IFRS basis 16,319 21,910

Adjustments to reconcile to US GAAP:

Reversal of capitalized product

development cost

-

(503 ) (535 )

Reversal of pensions and other

postretirement benefi ts

-

1,750 1,700

Goodwill amortization (until January 1, 2004) - 321 290

Goodwill capitalization (acquisition-related) - 40 30

Acquisition-related intangibles - (294 ) (210 )

Equity-accounted investees - 178 105

Reversal of result on recognition of sale

and leaseback

-

(80 ) (52 )

Deferred tax effect - (424 ) (168 )

Discontinued operations - (664 ) −

Provisions - − (58 )

Other - 23 (15 )

Stockholders’ equity as per the consolidated

balance sheets on a US GAAP basis

16,666 22,997

112 Group fi nancial statements 172 IFRS information

Notes to the IFRS fi nancial statements

218 Company fi nancial statements