General Motors 2012 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2012 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

In addition to the financing we provide through GM Financial, we also ensure availability of competitive financing for our

customers and dealers through operating relationships with financial institutions. Historically, Ally Financial provided a majority of

the financing for our dealers and a significant portion of the financing for our customers in the U.S., Canada and other major

international markets where we operate. Ally Financial continues to be the largest third-party provider of the financing for our dealers

and customers. We have added relationships with other financial institutions to increase our competitiveness and benefit from

additional financing sources, including arrangements to provide incentivized retail financing to our customers in the U.S., Canada,

U.K. and Australia.

Focus on Chinese Market

We view the Chinese market, the fastest growing global market by volume of vehicles sold, as important to our global growth

strategy and are employing a multi-brand strategy led by our Buick and Chevrolet brands. In the coming years we plan to increasingly

leverage our global architectures to increase the number of nameplates under the Buick, Chevrolet and Cadillac brands in China and

continue to grow our business under the Baojun, Jiefang and Wuling brands. We operate in Chinese markets through a number of joint

ventures and maintaining good relations with our joint ventures partners, which are affiliated with the Chinese government, is an

important part of our China growth strategy.

Refer to Note 10 to our consolidated financial statements for our direct ownership interests in our Chinese joint ventures,

collectively referred to as China JVs.

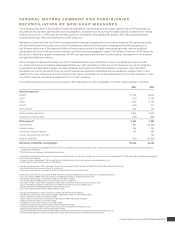

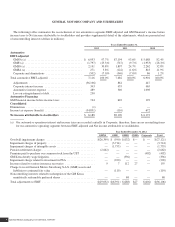

The following tables summarize certain key operational and financial data for the China JVs (dollars in millions, vehicles in

thousands):

Years Ended December 31,

2012 2011 2010

Total wholesale vehicles (a) ........................................ 2,909 2,573 2,348

Market share (b) ................................................. 14.6% 13.6% 12.8%

Total net sales and revenue ......................................... $33,364 $30,511 $25,395

Net income ..................................................... $ 3,198 $ 3,203 $ 2,808

December 31, 2012 December 31, 2011

Cash and cash equivalents ..................................................... $ 5,522 $ 4,679

Debt ....................................................................... $ 123 $ 106

(a) Including vehicles exported to markets outside of China.

(b) Market share for China market.

GME

During the second half of 2011 and continuing into 2012, the European automotive industry has been severely affected by the

ongoing sovereign debt crisis, high unemployment and a lack of consumer confidence coupled with overcapacity. European

automotive industry sales to retail and fleet customers were 19.0 million vehicles in 2012, representing a 5.6% decrease compared to

2011. In 2012 GME’s market share declined to 8.5% from 8.7% in 2011 and the region suffered EBIT (loss)-adjusted of $1.8 billion

in 2012 compared to EBIT (loss)-adjusted of $0.7 billion in 2011. During this timeframe, we began to experience deterioration in cash

flows.

In response, we formulated a plan to implement various actions to strengthen our operations and increase our competitiveness. The key

areas of the plan include investments in our product portfolio, a revised brand strategy, significant management changes, reducing material,

development and production costs, and further leveraging synergies from the alliance between us and Peugeot S.A. (PSA), as subsequently

discussed. The success of our plan will depend on a combination of our ability to execute the actions contemplated, as well as external

General Motors Company 2012 ANNUAL REPORT 21