General Motors 2012 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2012 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

Refer to Note 12 to our consolidated financial statements for additional information on Goodwill impairments, including

information pertaining to the determination of the fair values of our reporting units requiring a Step 2 analysis, and the risks of future

goodwill impairment charges.

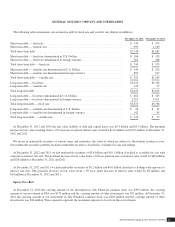

Subsequent to the recording of the Goodwill impairment charges in the year ended December 31, 2012 we had Goodwill of

$2.0 billion at December 31, 2012 which predominantly arose upon the acquisition of AmeriCredit Corp. compared to $29.0 billion at

December 31, 2011 which predominantly arose upon the application of fresh-start reporting. When applying fresh-start reporting,

certain accounts, primarily employee benefit and income tax related, were recorded at amounts determined under specific U.S. GAAP

rather than fair value, and the difference between the U.S. GAAP and fair value amounts gave rise to goodwill, which is a residual.

Our employee benefit related accounts were recorded in accordance with ASC 712, “Compensation - Nonretirement Postemployment

Benefits” (ASC 712) and ASC 715, “Compensation - Retirement Benefits” and deferred income taxes were recorded in accordance

with ASC 740, “Income Taxes.” The application of ASC 712 and 715 during fresh-start reporting resulted in our recorded liabilities

for certain employee benefit obligations being higher than the fair value of these obligations because lower discount rates were

utilized in determining the U.S. GAAP values compared to those utilized to determine fair values. The discount rates utilized to

determine the fair value of these obligations were based on our incremental borrowing rates, which included our nonperformance risk.

Our incremental borrowing rates are also affected by changes in market interest rates. Further, upon the application of fresh-start

reporting, the recorded amounts of our assets were lower than their fair values because of the recording of valuation allowances on

certain of our deferred tax assets, which under ASC 852 also resulted in goodwill. If all identifiable assets and liabilities had been

recorded at fair value upon application of fresh-start reporting, no goodwill would have resulted.

Since fresh-start reporting the differences between these fair value-to-U.S. GAAP amounts; (1) have decreased because of

decreases in credit spreads between high quality corporate bond rates and market interest rates for companies with similar

nonperformance risk; (2) have decreased due to improvements in our credit rating, thus resulting in a decrease in the spread between

our employee benefit related obligations under U.S. GAAP and their fair values; and/or (3) decreased due to a change in the fair

values of our estimated employee benefit obligations. Decreases also occurred from reversals of our deferred tax asset valuation

allowances. The fair value-to-U.S. GAAP differences decreases for these reasons have resulted in the decline of implied goodwill in

each of the years ended December 31, 2012 and 2011. At the next annual or event-driven goodwill impairment test, to the extent the

carrying amount of a reporting unit exceeds its fair value or the reporting unit has a negative carrying amount, a goodwill impairment

could occur. Future goodwill impairments could also occur should we reorganize our internal reporting structure in a manner that

changes the composition of one or more of our reporting units. Upon such an event, goodwill would be reassigned to the affected

reporting units using a relative-fair-value allocation approach, unless the entity was never integrated, and not based on the amount of

goodwill that was originally attributable to fair value-to-U.S. GAAP differences that gave rise to goodwill upon application of fresh-

start reporting.

For purposes of our 2012 annual impairment testing procedures at October 1, 2012, the estimated fair values of our more significant

reporting units exceeded their carrying amounts by 111.8% for GMNA, 57.9% for GM Mercosur and 14.7% for GM Financial. In

calculating the fair values of our more significant reporting units during our 2012 annual goodwill impairment testing, keeping all

other assumptions constant, the estimated fair values of our more significant reporting units would still exceed their carrying amounts

had our weighted-average cost of capital (WACC) increased by 1,000 basis points for GMNA and 160 basis points for GM Mercosur.

GM Financial’s forecasted equity-to-managed asset retention ratio by 2015 was 12.5% and held constant thereafter. GM Korea’s fair

value continued to be below its carrying amount. GM Financial’s fair value would still exceed its carrying amount had equity to

managed assets retention ratio increased 160 basis points by 2015. Subsequent to our 2012 annual goodwill impairment testing, we

reversed deferred tax asset valuation allowances of $36.2 billion for our GMNA reporting unit causing its carrying amount to exceed

its fair value. As a result we performed an event-driven goodwill impairment test in the three months ended December 31, 2012.

Based on our testing we determined that the differences between the fair value-to-U.S. GAAP amounts decreased primarily due to the

recorded amount of our deferred tax assets exceeding their fair values, which under ASC 805, “Business Combinations” results in less

implied goodwill. Based on this event-driven impairment test we recorded a Goodwill impairment charge of $26.4 billion in the year

ended December 31, 2012 within our GMNA segment.

General Motors Company 2012 ANNUAL REPORT 59