General Motors 2012 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2012 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

5

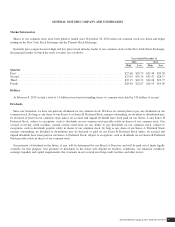

General Motors Company 2012 ANNUAL REPORT

These and other favorable trends prompted Canada’s

DBRS and Fitch Ratings to upgrade GM’s corporate

credit rating. DBRS now rates GM as investment

grade and all three major U.S. ratings agencies have

us rated one notch below investment grade. Our

target is to achieve investment grade across-the-

board as soon as possible and improve from there.

CREATING A SUSTAINABLE

COMPETITIVE ADVANTAGE

GM’s much improved financial structure and our

$23.2 billion in EBIT-adjusted since the beginning

of 2010 are allowing us to reinvest in the business

at a consistently high level, despite the fact that

most European economies are in distress and U.S.

sales remained below pre-recession levels in 2012.

Our capital expenditures increased from $6.2 billion

in 2011 to $8.1 billion in 2012, and I expect capital

spending will stay at about this level in coming years.

We can do this because of our low break-even point in

North America, the global geographic diversity of our

earnings and our fortress balance sheet.

Our operating results and financial discipline also

made it possible to execute a number of transactions

that will improve our competitive position and reduce

risk going forward.

•Through GM Financial, we are acquiring Ally

Financial’s International Operations in Europe

and Latin America, and Ally’s share of its China

joint venture. With the Ally acquisitions and GM

Financial’s other new business initiatives, we

will be able to provide financing in markets that

represent 80 percent of our sales volume. We

will also be able to meet demand in strategic and

underserved markets – all with very good risk-

adjusted returns and a smaller balance sheet than

other captive automotive finance companies.

•To ensure GM has state-of-the-art information

technology (IT), we are consolidating 23 mostly

leased and shared data centers around the

world into two fully redundant, company-owned

facilities. The next step is to transform IT into a

competitive advantage, so we are creating four

innovation centers to develop proprietary business

application software. Together, these moves will

give us the most robust applications, and the most

accurate, timely and secure data.

• In a particularly innovative set of transactions, we

reduced our U.S. salaried pension obligations by

$28 billion. By offering retirees a lump sum buy-out

or an insurance company-backed annuity, we were

able to reduce a form of leverage, reduce claims

on our future cash flow and actually enhance the

income security of our salaried retirees.

• Late in the year, we strengthened our fortress

balance sheet by replacing our existing $5 billion

revolving line of credit with two new credit

facilities totaling $11 billion. This additional

liquidity is appropriate for a company of our size.

But what made it a landmark deal was the fact

that we earned investment-grade pricing and

investment-grade terms and conditions – a clear

vote of confidence in the financial strength of

General Motors.

FIXING GM EUROPE

One of the urgent issues we

are addressing is the economic

crisis in Europe, which led to

increased losses in the region. I’m

encouraged that after several years

of restructuring, which intensified

in 2012, we are now seeing green

shoots. Indeed, our objective is to

achieve break-even EBIT-adjusted

results by mid-decade.

The foundation of our Europe

revitalization plan is to grow

Chevrolet and underpin Opel/

Vauxhall’s great new products with

a competitive cost structure and

the right “go to market” strategy.

Significant progress has been

made on all of these fronts:

•We continue to rationalize capacity and pursue

productivity gains. We announced the sale of our

transmission operations in Strasbourg, France,

and confirmed that car production will cease at our

plant in Bochum, Germany.

•We significantly strengthened our leadership team

in Europe, most notably with the appointment of

Dr. Karl-Thomas Neumann, a veteran Volkswagen

executive, as chairman of the Opel management

board and president of GM Europe. Dr. Neumann

started work on March 1, 2013.

$28B

Reduced U.S. salaried

pension liability

Capital expenditures

2011 $6.2B

$8.1B

2012