BB&T 2009 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

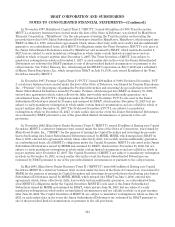

At December 31, 2009, none of the purchased impaired or purchased nonimpaired loans were classified as

nonperforming assets. Therefore, interest income, through accretion of the difference between the carrying

amount of the loans and the expected cash flows, is being recognized on all purchased loans. There was no

allowance for credit losses related to the purchased loans at December 31, 2009.

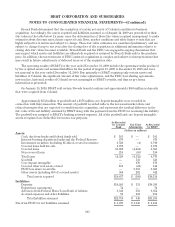

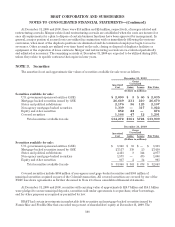

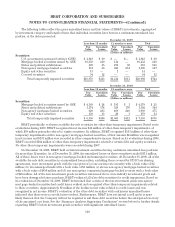

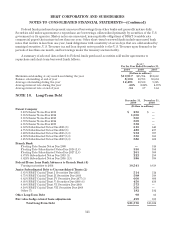

The following table provides details regarding BB&T’s investment in leveraged leases.

December 31,

2009 2008

(Dollars in millions)

Rentals receivable (net of principal and interest on nonrecourse debt and head lease

obligation) $ 750 $1,367

Unearned income (375) (614)

Investment in leveraged leases, net of unearned income 375 753

Deferred taxes arising from leveraged leases 12 (70)

Net investment in leveraged leases $ 387 $ 683

BB&T entered into a settlement agreement in 2008 with the Internal Revenue Service (“IRS”) regarding its

leveraged lease transactions. For tax purposes, the leveraged leases were deemed terminated as of December 31,

2008. Please refer to Note 13 for additional details regarding BB&T’s leveraged lease settlement.

BB&T had $73.6 billion in loans secured by real estate at December 31, 2009. However, these loans were not

concentrated in any specific market or geographic area other than Branch Bank’s primary markets. Certain loans

have been pledged as collateral for all outstanding Federal Home Loan Bank advances and certain other

corporate purposes at December 31, 2009 and 2008.

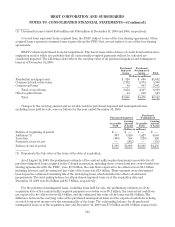

The following table sets forth certain information regarding BB&T’s impaired loans, excluding acquired

impaired loans, that were evaluated for specific reserves:

December 31,

2009 2008

(Dollars in millions)

Total recorded investment—impaired loans $1,598 $ 740

Total recorded investment with no related valuation allowance 611 145

Total recorded investment with related valuation allowance 987 595

Allowance for loan and lease losses assigned to impaired loans (176) (102)

Net carrying value—impaired loans $1,422 $ 638

Average impaired loans for the years ended December 31, 2009, 2008, and 2007 were $1.1 billion, $512 million

and $137 million, respectively. The amount of interest that has been recognized as income on impaired loans for

any of the last three years was not material.

At December 31, 2009, BB&T had $471 million in loans that were accruing interest under the terms of

troubled debt restructurings. This amount consists of $103 million in residential mortgage loans, $54 million in

revolving credit loans, $308 million in commercial loans and $6 million in direct retail loans. Loan restructurings

generally occur when a borrower is experiencing, or is expected to experience, financial difficulties in the near-

term. Consequently, a modification that would otherwise not be considered is granted to the borrower. These

loans may continue to accrue interest as long as the borrower complies with the revised terms and conditions and

has demonstrated repayment performance with the modified terms.

114