BB&T 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

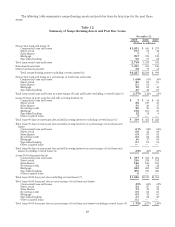

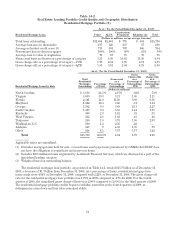

In addition, management has intentionally lowered its exposure to real estate lending over the past several years,

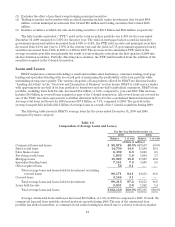

which has resulted in lower balances of commercial real estate loans. This has been offset by an increased focus on

commercial and industrial loans. BB&T experienced stronger trends in commercial and industrial lending in 2009

primarily in lending relationships with healthcare and governmental entities, due to BB&T’s strong capital

position, credit ratings and willingness to extend credit.

Average direct retail loans declined 5.5% in 2009 due to continuing difficulties in the residential real estate

market, which decreased demand for home equity loan products. Average sales finance loans and average

revolving credit reflected growth rates of 2.8% and 11.5% during 2009, respectively. BB&T concentrates its

efforts on the highest quality borrowers in both of these product markets.

Average mortgage loans held for investment decreased $1.4 billion, or 8.1%, compared to 2008. Management

views mortgage loans as an integral part of BB&T’s relationship-based credit culture. BB&T is a large originator

of residential mortgage loans, with 2009 originations of $28.2 billion. The vast majority of mortgage loans

originated during 2009 were conforming mortgage loans that were either sold in the secondary market or held in

the loans held for sale portfolio at year-end, which is the primary reason for the decline in mortgage loans held for

investment. Average loans held for sale, which primarily consists of government-conforming mortgage loans,

increased $1.5 billion, or 111.0% compared to 2008 as refinance activity significantly increased due to the

historically low loan rates for mortgages.

Average loans held by BB&T’s specialized lending subsidiaries increased $1.6 billion, or 29.6%, compared to

2008. The growth in the specialized lending portfolio was primarily in insurance premium finance lending,

equipment finance leases and automobile loans. This increase includes the acquisition of assets of an insurance

premium finance business on February 2, 2009, which added approximately $715 million in loans.

The average annualized FTE yield for 2009 for the total loan portfolio was 5.49% compared to 6.35% for the

prior year. The 86 basis point decline in the FTE yield on the loan portfolio was primarily the result of the

repricing of loans in response to the decreases in the prime lending rate and other indices, as well as a higher

level of nonperforming loans in 2009 as compared to 2008. These declines were partially offset by wider loan

spreads on new originations and the Colonial acquisition. The average prime rate in effect during 2009 and 2008

was 3.25% and 5.09%, respectively.

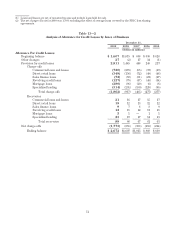

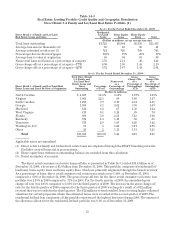

Asset Quality and Credit Risk Management

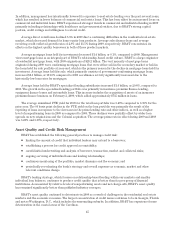

BB&T has established the following general practices to manage credit risk:

Šlimiting the amount of credit that individual lenders may extend to a borrower;

Šestablishing a process for credit approval accountability;

Šcareful initial underwriting and analysis of borrower, transaction, market and collateral risks;

Šongoing servicing of individual loans and lending relationships;

Šcontinuous monitoring of the portfolio, market dynamics and the economy; and

Šperiodically reevaluating the bank’s strategy and overall exposure as economic, market and other

relevant conditions change.

BB&T’s lending strategy, which focuses on relationship-based lending within our markets and smaller

individual loan balances, continues to produce credit quality that is better than its peer group of financial

institutions. As measured by relative levels of nonperforming assets and net charge-offs, BB&T’s asset quality

has remained significantly better than published industry averages.

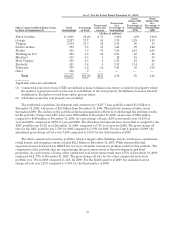

BB&T’s asset quality continued to deteriorate in 2009 as a result of challenges in the residential real estate

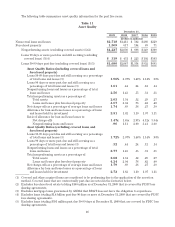

markets and the economic recession. The largest concentration of credit issues continues to be in Georgia, Florida

and metro Washington, D.C., which includes the surrounding suburbs. In addition, BB&T has experienced some

deterioration in the coastal areas of the Carolinas.

45