BB&T 2009 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

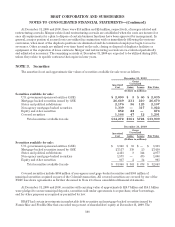

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

lending commitments at the balance sheet date. The Company determines the allowance for loan and lease losses

and the reserve for unfunded lending commitments based on an ongoing evaluation. This evaluation is inherently

subjective because it requires material estimates, including the amounts and timing of cash flows expected to be

received on impaired loans. Those estimates are susceptible to significant change. Changes to the allowance for

loan and lease losses and the reserve for unfunded lending commitments are made by charges to the provision for

credit losses, which is reflected in the Consolidated Statements of Income. Loans or lease balances deemed to be

uncollectible are charged off against the allowance for loan and lease losses. Recoveries of amounts previously

charged-off are credited to the allowance for loan and lease losses.

The allowance for loan and lease losses is the accumulation of various components that are calculated based

on various methodologies. BB&T’s allowance for loan and lease losses consists of (1) a component for individual

loan impairment, and (2) components of collective loan impairment.

BB&T maintains specific reserves for individually impaired loans. A loan is impaired when, based on current

information and events, it is probable that BB&T will be unable to collect all amounts due (interest as well as

principal) according to the contractual terms of the loan agreement. Specific reserves are determined on a loan by

loan basis based on management’s best estimate of BB&T’s exposure, given the current payment status of the

loan, the present value of expected payments and the value of any underlying collateral.

Management’s estimate of reserves established for collective impairment reflect losses inherent in the loan

and lease portfolios as of the balance sheet reporting date. Embedded loss estimates are based on current

migration rates and current risk mix. Embedded loss estimates may be adjusted to reflect current economic

conditions and current portfolio trends including credit quality, concentrations, aging of the portfolio, and

significant policy and underwriting changes.

For loans acquired in a business combination after December 31, 2008, BB&T has generally aggregated the

purchased loans into pools of loans with common risk characteristics. In determining the allowance for loan and

lease losses, BB&T performs analysis each period to estimate the expected cash flows for each of the loan pools.

To the extent that the expected cash flows of a loan pool have decreased since the acquisition date, BB&T

establishes an allowance for loan loss.

The methodology used to determine the reserve for unfunded lending commitments is inherently similar to

that used to determine the collective component of the allowance for loan and lease losses described above,

adjusted for factors specific to binding commitments, including the probability of funding and exposure at default.

While management uses the best information available to establish the allowance for loan and lease losses

and the reserve for unfunded lending commitments, future adjustments may be necessary if economic conditions

differ substantially from the assumptions used in performing the valuations or, if required by regulators, based

upon information available to them at the time of their examinations.

Premises and Equipment

Premises, equipment, capital leases and leasehold improvements are stated at cost less accumulated

depreciation or amortization. Land is stated at cost. In addition, purchased software and costs of computer

software developed for internal use are capitalized provided certain criteria are met. Depreciation and

amortization are computed principally using the straight-line method over the estimated useful lives of the

related assets. Leasehold improvements are amortized on a straight-line basis over the lesser of the lease terms,

including certain renewals that were deemed probable at lease inception, or the estimated useful lives of the

improvements. Capitalized leases are amortized by the same methods as premises and equipment over the

estimated useful lives or lease terms, whichever is less. Obligations under capital leases are amortized using the

interest method to allocate payments between principal reduction and interest expense. Rent expense and rental

income on operating leases is recorded using the straight-line method over the appropriate lease terms.

99