BB&T 2009 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

Liquidity

Liquidity represents BB&T’s continuing ability to meet funding needs, primarily deposit withdrawals, timely

repayment of borrowings and other liabilities, and funding of loan commitments. In addition to the level of liquid

assets, such as trading securities and securities available for sale, many other factors affect the ability to meet

liquidity needs, including access to a variety of funding sources, maintaining borrowing capacity in national

money markets, growing core deposits, the repayment of loans and the capability to securitize or package loans

for sale.

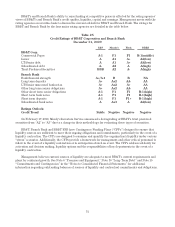

The purpose of the Parent Company is to serve as the capital financing vehicle for the operating subsidiaries.

The assets of the Parent Company consist primarily of cash on deposit with Branch Bank, equity investments in

subsidiaries, advances to subsidiaries, accounts receivable from subsidiaries, and other miscellaneous assets. The

principal obligations of the Parent Company are principal and interest on master notes, long-term debt, and

redeemable capital securities. The main sources of funds for the Parent Company are dividends and management

fees from subsidiaries, repayments of advances to subsidiaries, and proceeds from the issuance of long-term debt

and master notes. The primary uses of funds by the Parent Company are for the retirement of common stock,

investments in subsidiaries, advances to subsidiaries, dividend payments to shareholders, and interest and

principal payments due on long-term debt and master notes.

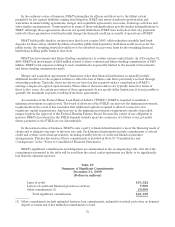

The primary source of funds used for Parent Company cash requirements has been net proceeds from the

issuance of long-term debt, which totaled $3.9 billion in 2009. In addition, dividends received from Branch Bank

and its subsidiaries totaled $459 million during 2009. Funds raised through master note agreements with

commercial clients are placed in a note receivable at Branch Bank primarily for its use in meeting short-term

funding needs and, to a lesser extent, to support the short-term temporary cash needs of the Parent Company. At

December 31, 2009 and 2008, master note balances totaled $1.0 billion and $1.7 billion, respectively.

The Parent Company had five issues of senior notes outstanding totaling $2.8 billion and five issues of

subordinated notes outstanding totaling $3.0 billion at December 31, 2009. In addition, as of December 31, 2009,

the Parent Company had $3.3 billion of junior subordinated debentures outstanding to unconsolidated trusts.

Please refer to Note 10 “Long-Term Debt” in the “Notes to Consolidated Financial Statements” for additional

information with respect to these senior notes, subordinated notes and junior subordinated debentures.

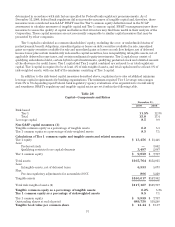

Branch Bank has several major sources of funding to meet its liquidity requirements, including access to

capital markets through issuance of senior or subordinated bank notes and institutional certificates of deposit,

access to the FHLB system, dealer repurchase agreements and repurchase agreements with commercial clients,

participation in the Treasury, Tax and Loan and Special Direct Investment programs with the Federal Reserve

Bank, access to the overnight and term Federal funds markets, use of a Cayman branch facility, access to retail

brokered certificates of deposit and a borrower in custody program with the Federal Reserve Bank for the

discount window. As of December 31, 2009, BB&T has approximately $39 billion of secured borrowing capacity,

which represents approximately 413% of one year wholesale funding maturities.

72