BB&T 2009 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

During 2009, 2008 and 2007, BB&T sold residential mortgage loans with unpaid principal balances of $25.8

billion, $13.4 billion and $7.5 billion, respectively, and recognized pretax gains of $357 million, $78 million and $12

million, respectively, which were recorded in noninterest income as a component of mortgage banking income.

BB&T retained the related mortgage servicing rights and receives servicing fees. At December 31, 2009 and

2008, the approximate weighted average servicing fee was .37% of the outstanding balance of the residential

mortgage loans. The weighted average coupon interest rate on the portfolio of mortgage loans serviced for others

was 5.57% and 6.03% at December 31, 2009 and 2008, respectively.

At December 31, 2009, BB&T had $2.0 billion of residential mortgage loans sold with limited recourse

liability. In the event of nonperformance by the borrower, BB&T has maximum recourse exposure of

approximately $667 million on these mortgage loans. At December 31, 2009, BB&T has recorded $6 million of

reserves related to these recourse exposures.

The Company also has securitized residential mortgage loans and retained the resulting securities available

for sale. As of December 31, 2009, the fair value of the securities available for sale still owned by BB&T was $62

million and the remaining unpaid principal balance of the underlying loans totaled $60 million. Based on the

performance of the underlying loans and general liquidity of the securities, the Company’s recovery of the cost

basis in the securities has not been significantly impacted by changes in interest rates, prepayment speeds or

credit losses.

Residential mortgage servicing rights are recorded on the Consolidated Balance Sheets at fair value with

changes in fair value recorded as a component of mortgage banking income in the Consolidated Statements of

Income for each period. BB&T uses various derivative instruments to mitigate the income statement effect of

changes in fair value, due to changes in valuation inputs and assumptions, of its residential mortgage servicing

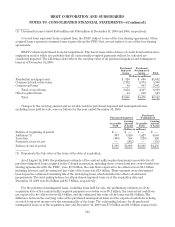

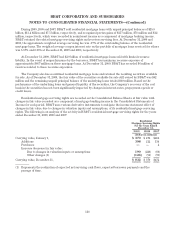

rights. The following is an analysis of the activity in BB&T’s residential mortgage servicing rights for the years

ended December 31, 2009, 2008 and 2007:

Residential

Mortgage Servicing Rights

For the Years Ended

December 31,

2009 2008 2007

(Dollars in millions)

Carrying value, January 1, $ 370 $ 472 $484

Additions 398 212 134

Purchases ——4

Increase (decrease) in fair value:

Due to changes in valuation inputs or assumptions 190 (220) (60)

Other changes (1) (126) (94) (90)

Carrying value, December 31, $ 832 $ 370 $472

(1) Represents the realization of expected net servicing cash flows, expected borrower payments and the

passage of time.

118