BB&T 2009 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

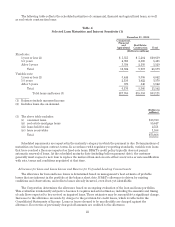

While management uses the best information available to establish the allowance for loan and lease losses,

future adjustments to the allowance or to the reserving methodology may be necessary if economic conditions

differ substantially from the assumptions used in making the valuations.

The following table presents an estimated allocation of the allowance for loan and lease losses at the end of

each of the past five years. This allocation of the allowance for loan and lease losses is calculated on an

approximate basis and is not necessarily indicative of future losses or allocations. The entire amount of the

allowance is available to absorb losses occurring in any category of loans and leases.

Table 5

Allocation of Allowance for Loan and Lease Losses by Lines of Business

December 31,

2009 2008 2007 2006 2005

Amount

% Loans

in each

category (1) Amount

% Loans

in each

category Amount

% Loans

in each

category Amount

% Loans

in each

category Amount

% Loans

in each

category

(Dollars in millions)

Balances at end of period

applicable to:

Commercial loans and

leases $1,574 52.1% $ 912 51.9% $ 548 49.3% $475 49.8% $422 49.2%

Sales finance 77 6.6 55 6.5 58 6.6 58 6.9 65 7.1

Revolving credit 127 2.1 94 1.8 70 1.8 67 1.7 65 1.8

Direct retail 297 15.0 124 15.9 79 17.3 75 18.5 94 19.4

Residential mortgage loans 131 16.2 91 17.6 25 19.2 21 18.8 19 18.8

Specialized lending 264 8.0 238 6.3 171 5.8 139 4.3 110 3.7

Unallocated 130 — 60 — 53 — 53 — 50 —

Total $2,600 100.0% $1,574 100.0% $1,004 100.0% $888 100.0% $825 100.0%

(1) Excludes loans covered by FDIC loss sharing agreements.

Investment Activities

Investment securities represent a significant portion of BB&T’s assets. Branch Bank invests in securities as

allowable under bank regulations. These securities include obligations of the U.S. Treasury, U.S. government

agencies, U.S. government-sponsored entities, including mortgage-backed securities, bank eligible obligations of

any state or political subdivision, privately-issued mortgage-backed securities, structured notes, bank eligible

corporate obligations, including corporate debentures, commercial paper, negotiable certificates of deposit,

bankers acceptances, mutual funds and limited types of equity securities. Branch Bank also may deal in securities

subject to the provisions of the Gramm-Leach-Bliley Act. Scott & Stringfellow, LLC, BB&T’s full-service

brokerage and investment banking subsidiary, engages in the underwriting, trading and sales of equity and debt

securities subject to the risk management policies of the Corporation.

BB&T’s investment activities are governed internally by a written, board-approved policy. The investment

policy is carried out by the Corporation’s Market Risk and Liquidity Committee (“MRLC”), which meets

regularly to review the economic environment and establish investment strategies. The MRLC also has much

broader responsibilities, which are discussed in the “Market Risk Management” section in “Management’s

Discussion and Analysis of Financial Condition and Results of Operations” herein.

Investment strategies are reviewed by the MRLC based on the interest rate environment, balance sheet

mix, actual and anticipated loan demand, funding opportunities and the overall interest rate sensitivity of the

Corporation. In general, the investment portfolio is managed in a manner appropriate to the attainment of the

following goals: (i) to provide a sufficient margin of liquid assets to meet unanticipated deposit and loan

fluctuations and overall funds management objectives; (ii) to provide eligible securities to secure public funds,

trust deposits as prescribed by law and other borrowings; and (iii) to earn the maximum return on funds invested

that is commensurate with meeting the requirements of (i) and (ii).

24