BB&T 2009 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

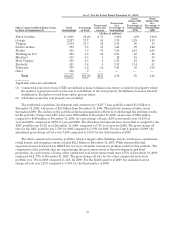

Substantially all of the loans acquired in the Colonial acquisition are covered by loss sharing agreements with

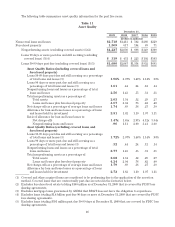

the FDIC, whereby the FDIC reimburses BB&T for the majority of the losses incurred. In addition, all of the

loans acquired were recorded at fair value as of the acquisition date without regard to the loss sharing

agreements. Loans were evaluated and assigned to loan pools based on common risk characteristics. The

determination of the fair value of the loans resulted in a significant write-down in the carrying amount of the

loans, which was assigned to an accretable or nonaccretable balance, with the accretable balance being recognized

as interest income over the remaining term of the loan. In accordance with the acquisition method of accounting,

there was no allowance brought forward on any of the acquired loans, as the credit losses evident in the loans

were included in the determination of the fair value of the loans at the acquisition date and are represented by the

nonaccretable balance. The majority of the nonaccretable balance is expected to be received from the FDIC in

connection with the loss share agreements and is recorded as a separate asset from the covered loans and

reflected on the Consolidated Balance Sheets. As a result, all of the loans acquired in the Colonial acquisition

were considered to be accruing loans as of the acquisition date. In accordance with regulatory reporting

standards, covered loans that are contractually past due will continue to be reported as past due and still accruing

based on the number of days past due. Because of the significant difference in the accounting for the covered

loans and the loss share agreements with the FDIC, management believes that asset quality measures excluding

the covered loans are generally more meaningful. Therefore, management has presented asset quality measures

in Table 11 that both include and exclude the covered loans and foreclosed property.

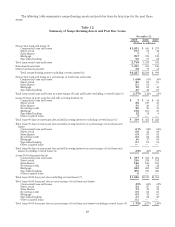

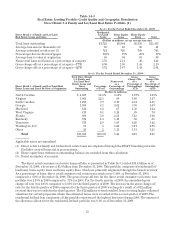

Nonperforming assets consist of foreclosed real estate, repossessions, nonaccrual loans and certain

restructured loans, which totaled $4.4 billion at December 31, 2009 (or $4.2 billion excluding covered foreclosed

property), compared to $2.0 billion at December 31, 2008. The increase in nonperforming assets included an

increase of $1.3 billion in nonperforming loans and $1.1 billion in foreclosed assets, including $160 million in

foreclosed property from the Colonial acquisition that is covered by the FDIC loss share agreements. Housing

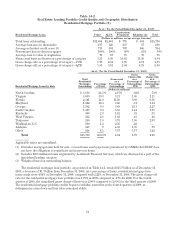

related projects accounted for 84% (52% for land/lots and 32% for 1-4 family homes) of total foreclosed property at

December 31, 2009. The increase in foreclosed properties was dispersed throughout BB&T’s markets, with the

largest increases occurring in Georgia, North Carolina, and Florida. As a percentage of loans and leases plus

foreclosed property, nonperforming assets were 4.07% at December 31, 2009 (or 4.24% excluding covered loans

and foreclosed property) compared with 2.04% at December 31, 2008.

Troubled debt restructurings generally occur when a borrower is experiencing, or is expected to experience,

financial difficulties in the near-term. As a result, BB&T will work with the borrower to prevent further

difficulties, and ultimately to improve the likelihood of recovery on the loan. To facilitate this process, a

concessionary modification that would not otherwise be considered may be granted resulting in classification as a

troubled debt restructuring. Troubled debt restructurings can involve loans remaining on non-accrual, moving to

non-accrual, or continuing on accruing status, depending on the individual facts and circumstances of the

borrower. Generally, a nonaccrual loan that is restructured remains on nonaccrual for a period of six months to

demonstrate the borrower can meet the restructured terms. However, performance prior to the restructuring, or

significant events that coincide with the restructuring, are considered in assessing whether the borrower can

meet the new terms and may result in the loan being returned to accrual status after a shorter performance

period. If the borrower’s ability to meet the revised payment schedule is not reasonably assured, the loan remains

classified as a nonaccrual loan.

The majority of BB&T’s loan modifications relate to commercial lending and involve extending the term of

the loan. In these cases, BB&T does not typically lower the interest rate or forgive principal or interest as part of

the loan modification. In addition, it is common for BB&T to obtain additional collateral or guarantor support

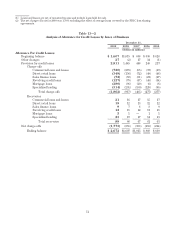

when modifying a loan. At December 31, 2009, BB&T had $471 million in loans that were accruing interest under

the terms of troubled debt restructurings. This amount consists of $308 million in commercial loans, $103 million

in residential mortgage loans, $54 million in revolving credit loans and $6 million in direct retail loans. Nonaccrual

restructured loans and leases are included in nonaccrual loans and leases in the accompanying tables. The amount

of loan restructurings has increased during 2009, as BB&T continues to work with borrowers who are

experiencing financial difficulties. As a result of continued economic stress, BB&T anticipates that it will have

further increases in loan restructurings during 2010.

47