BB&T 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

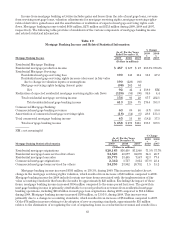

corresponding increase in personnel expense. The net change in the valuation of mortgage servicing rights

resulted in a $38 million increase compared to 2007. Excluding the impact of these items, mortgage banking

income increased $48 million, or 43.2%, compared to 2007. The growth in mortgage banking income for 2008

compared to 2007 includes strong production revenues from both residential and commercial mortgage banking

operations. The growth in commercial mortgage banking revenues was the result of the acquisition of Collateral

Real Estate Capital, LLC (“Collateral”) in the fourth quarter of 2007. BB&T combined the operations of

Collateral with its existing commercial mortgage banking operations and renamed the subsidiary Grandbridge

Real Estate Capital LLC (“Grandbridge”). The acquisition of Collateral significantly expanded the size and

product offerings of BB&T’s commercial mortgage banking activities.

BB&T recognized $199 million in net securities gains during 2009 compared to net gains of $107 million and

net losses of $3 million during 2008 and 2007, respectively. The net securities gains recognized in 2009 included

$240 million of net gains realized from securities sales and $41 million of losses as a result of other-than-

temporary impairments. The net securities gains recognized in 2008 included $211 million of net gains from

securities sales and $104 million of losses as a result of other-than-temporary impairments.

Income from bank owned life insurance (“BOLI”) increased $13 million, or 15.5%, in 2009 compared to 2008,

primarily due to a valuation adjustment in the prior year that resulted from a decline in the underlying assets of

certain insurance policies. BOLI income decreased $17 million, or 16.8%, in 2008 compared to 2007.

Other income increased $58 million, or 65.9%, in 2009 compared to 2008, primarily due to a $74 million

increase in the value of various financial assets isolated for the purpose of providing post-employment benefits.

The increase in the value of these assets is neutral to net income as these gains relate to participant’s accounts

and increase the amount of benefits that will be paid in the future. The current year also included a $27 million

gain on the sale of BB&T’s payroll processing business. Trading gains at Scott & Stringfellow increased $25

million and BB&T recognized $23 million in accretion on the FDIC loss share asset. These increases were

partially offset by $80 million in gains in 2008 related to BB&T’s ownership interest and sale of Visa, Inc. stock.

The slight decrease in 2008 compared to 2007 was driven by several factors. As mentioned above, other income in

2008 included gains related to BB&T’s ownership interest and sale of Visa, Inc. stock that amounted to $80

million. In addition, revenues from client derivative activities were $22 million higher in 2008 compared to 2007.

These increases were offset by a number of factors, including a $50 million decline in the value of various financial

assets isolated for the purpose of providing post-employment benefits. The decline in the value of these assets is

neutral to net income as these losses relate to participant’s accounts and reduce the amount of benefits that will

be paid in the future. Earnings from investments in low income housing partnerships that generate tax benefits

declined $39 million and net revenues from BB&T’s venture capital investments declined $26 million. In addition,

the change in results for 2008 compared to 2007 were affected by certain items that occurred in 2007, including a

gain of $19 million on the sale of an insurance operation and $33 million in losses from capital markets activities

due to disruptions in the financial markets that decreased the value of certain trading securities and derivative

contracts.

The ability to generate significant amounts of noninterest revenue in the future will be very important to the

continued financial success of BB&T. Through its subsidiaries, BB&T will continue to focus on asset management,

mortgage banking, trust, insurance, investment banking and brokerage services, as well as other fee-producing

products and services. BB&T plans to continue to pursue acquisitions of additional financial services companies,

including insurance agencies and other fee income producing businesses as a means of expanding fee-based

revenues. Also, among BB&T’s principal strategies following the acquisition of a financial institution is the cross-

sell of noninterest income generating products and services to the acquired institution’s client base. As previously

mentioned, management has set a goal to increase the contribution of noninterest revenue sources to 45% of total

income over the next few years.

64