BB&T 2009 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

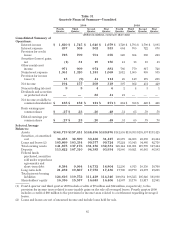

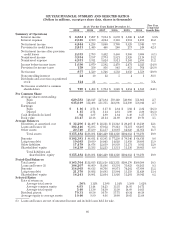

related to BB&T’s operating segments, the internal accounting and reporting practices used to manage these

segments and financial disclosures for these segments. Fluctuations in noninterest income and noninterest

expense incurred directly by the segments are more fully discussed in the “Noninterest Income” and

“Noninterest Expense” sections of this discussion and analysis.

Banking Network

The Banking Network had solid internal deposit growth, while the loan portfolios declined slightly due to the

general economic conditions and lack of strong demand for lending products during 2009. The total Banking

Network was composed of 1,857 banking offices at the end of 2009, an increase of 346 offices compared to 1,511

banking offices at December 31, 2008. The increase in offices was the result of the FDIC-assisted acquisition of

Colonial as well as a de novo branching strategy to expand BB&T’s presence in high growth markets. Net income

attributable to the Banking Network declined $644 million, or 61.1%, compared to 2008, primarily as a result of

higher provision for loan loss expense, credit related expenses primarily in owned real estate expense and FDIC

insurance premiums. Comparing 2008 to 2007, net income in the Banking Network decreased $584 million, or

35.7%.

Net interest income for the Banking Network totaled $3.6 billion in 2009 compared to $3.2 billion in 2008. The

increase in net interest income was primarily due to an increase of $807 million in the net funds transfer pricing

(“FTP”) provided to the Banking Network during 2009, offset by a decrease of $481 million in net interest income

from clients. The decline in net interest income from clients in 2009 compared to 2008 was primarily due to lower

interest income on loans resulting from the sustained historically low prime rate and increased non-accrual loan

balances, partially offset through controlling liability costs. It is important to note that the acquired loan portfolio

is covered by the loss sharing agreement under the terms of the Colonial acquisition and managed outside of the

Banking Network. The assets and related interest income from this portfolio are included in the Parent/

Reconciling Items segment. New loans originated by the acquired Colonial branches after August 14, 2009 will be

managed as part of the Banking Network and the associated income will be included in this segment on a

go-forward basis. Net interest income earned for 2008 declined by $209 million, or 6.1%, compared to 2007. The

decline in the net interest income was primarily due to lower interest income on loans resulting from the decline

in the prime rate that began in late 2007.

The economic provision for loan and lease losses increased $1.0 billion, or 123.1%, in 2009 compared to 2008,

reflecting the continued deterioration in the residential acquisition and development and commercial real estate

portfolios. The economic provision for loan and lease losses increased $685 million, or 441.9%, from 2007 to 2008.

The increase during 2008 reflected the deterioration in the residential acquisition and development portfolio, as

well as growth in outstanding loans.

Noninterest income in the Banking Network increased $58 million, or 4.7%, during 2009. The acquisition of

the Colonial branches contributed $44 million in noninterest income to the Banking Network. The remaining

increase in noninterest income was primarily due to growth in bankcard fees, loan fees, and checkcard fees. In

2008, noninterest income increased $140 million, or 12.8%, primarily due to growth in overdraft fees, checkcard

fees, and other nondeposit fees and commissions. Noninterest income allocated from other segments, which is

reflected as intersegment net referral fees (“referral fees”), increased $207 million, or 81.5%, and $15 million, or

6.3%, in 2009 and 2008, respectively, primarily due to higher referrals for mortgage lending. Noninterest

expenses incurred within the Banking Network during 2009 increased $537 million, or 34.8%, compared to 2008.

The acquisition of the Colonial branches created $160 million of additional noninterest expense in 2009 for the

Banking Network. The remaining increase of $377 million was primarily due to the increase in credit related

expenses primarily in owned real estate expense and FDIC insurance premiums. Comparing 2008 to 2007,

noninterest expenses increased $72 million, or 4.9%. Allocated corporate expenses increased $6 million, or 0.9%, in

2009. Comparing 2008 to 2007, allocated corporate expenses increased $112 million, or 19.0%, primarily due to

increased allocations for certain corporate overhead functions that were previously not allocated to the business

units, and increases for loan administration expense, IT services and operations. The increase related to loan

administration expense was the result of a change in the methodology for allocating these expenses between

business segments.

Total identifiable assets for the Banking Network decreased $2.3 billion in 2009, or 3.6%, to a total of $62.8

billion, compared to an increase of $4.5 billion, or 7.3%, in 2008. The loan portfolios declined slightly due to the

80