BB&T 2009 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2009 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

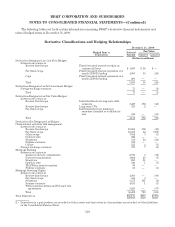

reflecting a fair value of $66 million recorded in other assets and instruments in a loss position reflecting a fair

value of $26 million recorded in other liabilities. For a qualifying cash flow hedge, the portion of changes in the

fair value of the derivatives that have been highly effective are recognized in other comprehensive income until

the related cash flows from the hedged item are recognized in earnings. The impact on earnings resulting from

the ineffectiveness of cash flow hedges was $1 million during 2009.

Accumulated other comprehensive income included $54 million in unrecognized after-tax gains on interest

rate swaps, caps and floors hedging variable interest payments on business loans at December 31, 2009. These

amounts included unrecognized after-tax gains on terminated swaps, caps and collars of $29 million at

December 31, 2009. In addition, accumulated other comprehensive income included $50 million in net

unrecognized after-tax gains on interest rate swaps, caps and floors hedging variable interest payments on

funding at December 31, 2009. These amounts included unrecognized after-tax gains on terminated hedges

related to short-term funding of $52 million at December 31, 2009. Also included in accumulated other

comprehensive income at December 31, 2009 are unrecognized after-tax gains of $3 million on terminated interest

rate swaps hedging variable interest payments on long-term debt.

The estimated net amount in accumulated other comprehensive income at December 31, 2009 that is

expected to be reclassified into earnings within the next 12 months is a net after-tax gain of $60 million. The

amount reclassified into earnings from other comprehensive income during 2009 was a net after-tax gain of $49

million.

All of BB&T’s cash flow hedges are hedging exposure to variability in future cash flows for forecasted

transactions related to the payment of variable interest on then existing financial instruments. The maximum

length of time over which BB&T is hedging its exposure to the variability in future cash flows for forecasted

transactions related to variable interest payments on existing financial instruments is 6.6 years.

Fair Value Hedges

At December 31, 2009, BB&T had designated notional values of $4.1 billion of derivatives as fair value hedges

which reflected a net unrealized gain of $101 million, with instruments in a gain position reflecting a fair value of

$194 million recorded in other assets and instruments in a loss position reflecting a fair value of $93 million

recorded in other liabilities. For a qualifying fair value hedge, changes in the value of the derivatives that have

been highly effective as hedges are recognized in current period earnings along with the corresponding changes

in the fair value of the designated hedged item attributable to the risk being hedged. BB&T terminated certain

fair value hedges relating to its long-term debt during 2009. The proceeds received from these terminations

totaled $128 million and were included in cash flows from financing activities. The impact on earnings resulting

from fair value hedge ineffectiveness was a $7 million gain during 2009.

BB&T also held $56.5 billion in notional value of derivatives not designated as hedges at December 31, 2009.

These instruments were in a net gain position with a net estimated fair value of $143 million. Changes in the fair

value of these derivatives are reflected in current period earnings.

Derivatives not designated as a hedge include the notional amount of $8.2 billion that have been entered into

as a risk management instrument for mortgage banking operations at December 31, 2009. For mortgage loans

originated for sale, BB&T is exposed to changes in market rates and conditions subsequent to the interest rate

lock and funding date. BB&T’s risk management strategy related to its interest rate lock commitment derivatives

and loans held for sale includes using mortgage-based derivatives such as forward commitments and options in

order to mitigate market risk.

Derivatives not designated as a hedge include the notional amount of $18.3 billion that have been entered

into as a risk management instrument for mortgage servicing rights at December 31, 2009. For 2009, the $98

million loss on these derivatives is offset by a positive $190 million valuation adjustment related to the mortgage

servicing asset.

152