Philips 2005 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2005 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

Philips Annual Report 2005 113

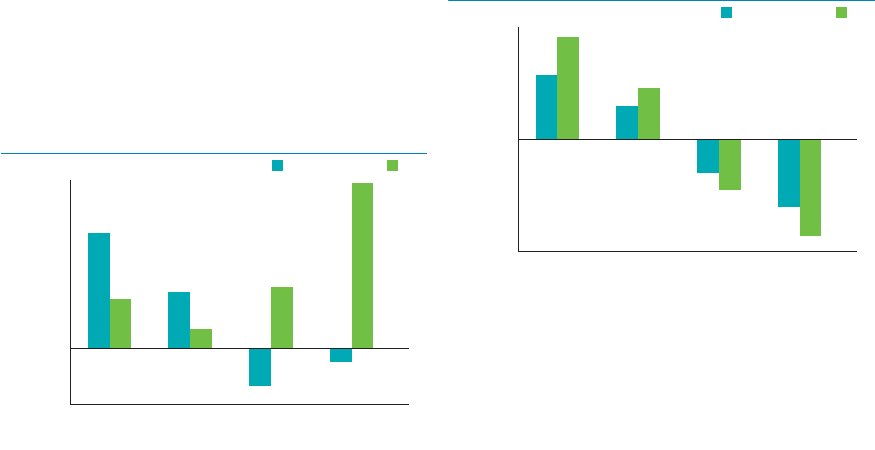

even big enough to cause a change in sign compared to

2004. This is related to the fact that the impact of interest

rate increases on NPPC for the UK is reduced by some

non-linearities in the recognition of gains and losses in

accordance with the applicable accounting standards.

Sensitivity of the net periodic pension cost to

simultaneous changes in interest rates and discount rates

2004 2005

Change in NPPC

(compared to total NPPC)

Change in interest rate

12%

10%

8%

6%

4%

2%

0%

(2%)

(4%)

(1.0%) (0.5%) 0.5% 1.0%

As the effects on interest cost and service costs from

changes in interest rates partially offset each other, and

changes in equity valuations do not affect either of them,

the interest rate and equity price sensitivities of NPPC are

largely determined by the sensitivities of the expected

returns on assets and the amortizations of unrecognised

gains and losses. Moreover, where these sensitivities have

opposite signs for changes in interest rates, they come on

top of each other for changes in equity valuations.

Consequently, the impact of changes in equity prices on

NPPC clearly exceeds that of changes in interest rates.

As with the impact of interest rate changes, the impact of

changes in equity valuations on NPPC is the largest for the

Netherlands, where equity investments compared to the

Company’s total pension liabilities are largest. Declines

(increases) in equity prices lead to signifi cantly higher (lower)

NPPC levels. The increase in plan assets in 2005 compared

to 2004 and the resultant increase in the absolute sizes of

any percentage change in equity valuations as well as the

decline in estimated NPPC for 2006 compared to 2005

imply an increased sensitivity of NPPC to changes in

equity prices.

Sensitivity of the net periodic pension cost to changes in

equity valuations

2004 2005

Change in NPPC

(compared to total NPPC)

Change in equity valuations

80%

60%

40%

20%

0%

(20%)

(40%)

(60%)

(80%)

(20%) (10%) 10% 20%

While the exposure of the balance sheet to pension risk

has changed only minimally, the income statement has

become somewhat more exposed to it. This is largely

due to increased assets and liabilities. In percentage terms,

the increased sensitivity also results from the decline in

expected NPPC. Plan changes and changes in investment

policies have not been signifi cant enough to cause material

effects in this respect.

Fiscal

Philips is, as mentioned before, exposed to fi scal risks.

This section further describes this exposure.

Transfer pricing risks

Philips has issued transfer pricing directives, which are in

accordance with guidelines of the Organization of Economic

Co-operation and Development. As transfer pricing has

a cross-border effect, the focus of local tax authorities on

implemented transfer pricing procedures in a country may

have an impact on results in another country. In order to

mitigate the transfer pricing risks, audits are executed on

a regular basis to safeguard the correct implementation of

the transfer pricing directives.

Tax risk on general service agreements

Due to the centralization of certain activities in a limited

number of countries (such as research and development

costs, centralized costs for IT, and costs for corporate

functions and head offi ce) costs are also centralized. As a

consequence, for tax reasons these costs must be allocated

to the benefi ciaries, being the various Philips entities. For

that purpose general service agreements (GSAs) are

signed with a large number of entities. Tax authorities

review the implementation of GSAs, often auditing on

benefi t test for a particular country or the use of tax

credits attached to GSAs and royalty payments, and may