Philips 2005 Annual Report Download - page 186

Download and view the complete annual report

Please find page 186 of the 2005 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

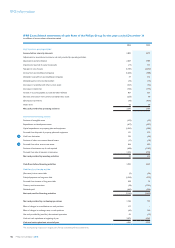

Philips Annual Report 2005186

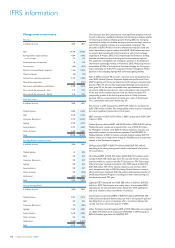

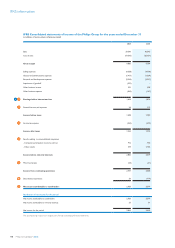

IFRS accounting policiesaccounting policies

Theconsolidatednancialstatementsinthissectionhavebeen

prepared in accordance with International Financial Reporting Standards

(IFRS) and its interpretations adopted by the EU. This is for the

Company materially the same as and in accordance with IFRS as

adopted by the International Accounting Standards Board (IASB). IFRS

include both IFRS and International Accounting Standards (IAS). These

aretheCompany’srstconsolidatednancialstatementsunderIFRS

and IFRS 1 ‘First-time Adoption of International Financial Reporting

Standards’ has been applied. An explanation of how the transition from

nancialstatementspreparedunderpreviousDutchlawtoIFRShas

affectedthereportednancialposition,nancialperformanceandcash

owsoftheCompanyisprovidedonpage191.

Historical cost is used as the measurement basis unless otherwise

indicated.

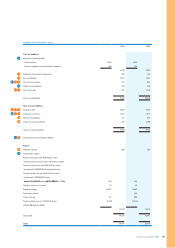

Consolidation principles

Theconsolidatednancialstatementsincludetheaccountsof

Koninklijke Philips Electronics N.V. (the ‘Company’) and all subsidiaries

thatfallunderitspowertogovernthenancialandoperatingpoliciesof

anentitysoastoobtainbenets

from its activities. The Company applies IAS 27 ‘Consolidated and

Separate Financial Statements’ and Interpretation SIC 12 ‘Consolidation

– Special Purpose Entities’. All intercompany balances and transactions

havebeeneliminatedintheconsolidatednancialstatements.

Net income is reduced by the portion of the earnings of subsidiaries

applicable to minority interests. The minority interests are disclosed

separately in the consolidated statements of income and in the

consolidated balance sheets.

Investments in unconsolidated companies

Investments in companies in which the Company does not have

theabilitytodirectlyorindirectlycontrolthenancialandoperating

decisions,butdoespossesstheabilitytoexertsignicantinuence,are

accounted for using the equity method. Generally, in the absence of

demonstrableproofofsignicantinuence,itispresumedtoexistifat

least 20% of the voting stock is owned. The Company’s share of the net

income of these companies is included in results relating to unconsolidated

companies in the consolidated statements of income. The Company

recognizes an impairment loss when the recoverable amount of the

investment is less than its carrying amount, in compliance with IAS 36

‘Impairment of Assets’. When the Company’s share of losses exceeds

its interest in an associate, the Company’s carrying amount of that

associate is reduced to nil and recognition of further losses is discontinued

except to the extent that the Company has incurred legal or constructive

obligations or made payments on behalf of an associate.

Accounting for capital transactions of a subsidiary or an

unconsolidated company

The Company recognizes dilution gains or losses arising from the sale

or issuance of stock by a consolidated subsidiary or an unconsolidated

entity which the Company is accounting for using the equity method

of accounting in the income statement, unless the Company or the

subsidiary either has reacquired or plans to reacquire such shares.

In such instances, the result of the transaction will be recorded directly

in equity as a non-operating gain or loss.

The dilution gains or losses are presented in the income statement

under Other business income (expenses) if they relate to consolidated

subsidiaries. Dilution gains and losses related to unconsolidated companies

are presented under Results relating to unconsolidated companies.

Foreign currencies

Thenancialstatementsofforeignentitiesaretranslatedintoeuros.

Assets and liabilities are translated using the exchange rates on the

respective balance sheet dates. Income and expense items in the income

statementandcashowstatementaretranslatedatweightedaverage

exchange rates during the year. The resulting translation adjustments

are recorded as a separate component of equity. Cumulative translation

adjustments are recognized as income or expense upon partial or

complete disposal or substantially complete liquidation of a foreign entity.

The functional currency of foreign entities is generally the local currency,

unless the primary economic environment requires the use of another

currency. Gains and losses arising from the translation or settlement of

foreign currency-denominated monetary assets and liabilities into the

local currency are recognized in income in the period in which they

arise. However, currency differences on intercompany loans that have

the nature of a permanent investment are accounted for as translation

differences as a separate component of equity.

Derivativenancialinstruments

TheCompanyusesderivativenancialinstrumentsprincipallyin

the management of its foreign currency risks and to a more limited

extent for interest rate and commodity price risks. In compliance

with IAS No. 39, ‘Financial Instruments’, which is early adopted as

fromJanuary1,2004,theCompanymeasuresallderivativenancial

instruments based on fair values derived from market prices of the

instruments or from option pricing models, as appropriate. Gains or

losses arising from changes in the fair value of the instruments are

recognized in the income statement during the period in which they

arise to the extent that the derivatives have been designated as a hedge

of recognized assets or liabilities, or to the extent that the derivatives

have no hedging designation or are ineffective. The gains and losses on

the designated derivatives substantially offset the changes in the values

of the recognized hedged items, which are also recognized as gains and

losses in the income statement. Changes in the fair value of a derivative

thatishighlyeffectiveandthatisdesignatedandqualiesasafairvalue

hedge, along with the loss or gain on the hedged asset, or liability or

unrecognizedrmcommitmentofthehedgeditemthatisattributable

to the hedged risk, are recorded in the income statement.

Changes in the fair value of a derivative that is highly effective and that

isdesignatedandqualiesasacashowhedge,arerecordedinequity,

untilprotorlossareaffectedbythevariabilityincashowsofthe

designated hedged item. Changes in the fair value of derivatives that

are highly effective as hedges and that are designated and qualify as

foreigncurrencyhedgesarerecordedineitherprotorlossorequity,

depending on whether the hedge transaction is a fair value hedge or

acashowhedge.

The Company formally assesses, both at the hedge’s inception and on an

ongoing basis, whether the derivatives that are used in hedging transactions

arehighlyeffectiveinoffsettingchangesinfairvaluesorcashowsof

hedged items. When it is established that a derivative is not highly

effective as a hedge or that it has ceased to be a highly effective hedge,

the Company discontinues hedge accounting prospectively. When hedge

accounting is discontinued because it has been established that the

derivativenolongerqualiesasaneffectivefairvaluehedge,theCompany

continues to carry the derivative on the balance sheet at its fair value,

and no longer adjusts the hedged asset or liability for changes in fair value.

When hedge accounting is discontinued because it is probable that a

forecasted transaction will not occur within a period of two months

from the originally forecasted transaction date, the Company continues

to carry the derivative on the balance sheet at its fair value, and gains

and losses that were accumulated in equity are recognized immediately

in the income statement. In all other situations in which hedge accounting

is discontinued, the Company continues to carry the derivative at its fair

value on the balance sheet, and recognizes any changes in its fair value in

the income statement. For interest rate swaps that are unwound, the

gain or loss upon unwinding is released to income over the remaining

lifeoftheunderlyingnancialinstruments,basedontherecalculated

effective yield.

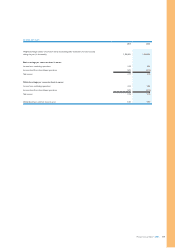

Cash and cash equivalents

Cash and cash equivalents include all cash balances and short-term

highly liquid investments with an original maturity of three months or

less that are readily convertible into known amounts of cash. They are

stated at face value.

IFRS information